")

")

Introduction

At the 4th of April I published an article about BE Semiconductor (OTC:BESIY) as a great long term holding in a dividend (growth) portfolio.

Since then a lot has happened with the share price. The stock price at publication was €79.2 and only a few months later the stock went way up to €110.40. It is no surprise this had to do with artificial intelligence (AI).

BESIY is one of those stocks that can benefit from the AI megatrend. In my other article about BESIY I wrote about hybrid bonding as the biggest catalyst of the company. Hybrid bonding will play an important role in the AI megatrend and can possibly accelerate earnings growth and enhancing profitability for the company.

Why BESIY?

BESIY is a Dutch semiconductor equipment manufacturer with a market cap of €8.96 billion. The company is fairly small, especially compared to the Dutch semiconductor giant ASML Holding N.V. (ASML). ASML is getting a lot attention internationally, and rightly so. However, I think BESIY also deserves a spot on your watch list because this company has a lot of long-term potential.

Shares are listed on Euronext Amsterdam and the level 1 ADRs trade on the OTC markets (OTC:BESIY). I highly encourage you to buy the shares on Euronext Amsterdam for liquidity reasons.

At the moment BESIY is one of the largest holdings in my portfolio and here is a summary why I think it is a high-quality business.

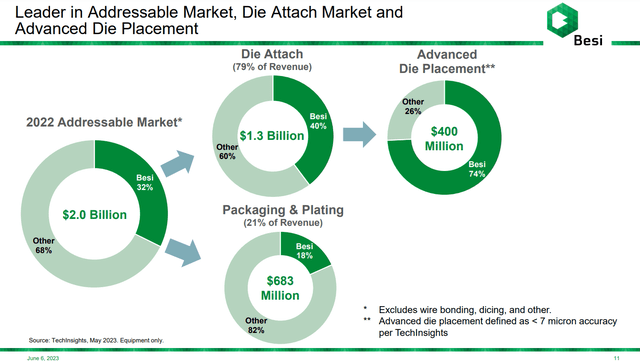

BESIY is one of the world leaders in the “back-end” part of the chip manufacturing process and they are still increasing market share in the “die attach” segment. Especially in the Advanced Die Placement BESIY has an impressive market share of 74%. The picture below shows that BESIY is ahead of its competitors when it comes to the more Advanced Die Placement equipment.

Since the Die Placement will be more and more complex in the future, it is possible that BESIY can expand its market leading position, which is good to see.

BESIY operating segment (Investor presentation)

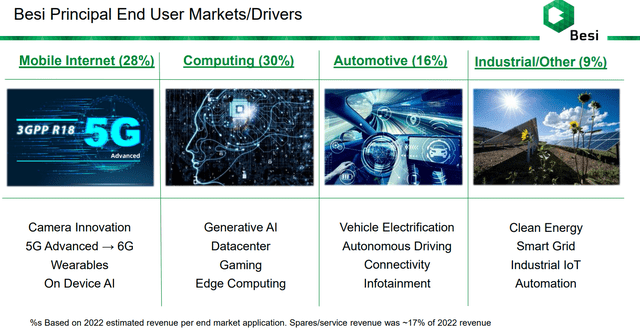

The company is involved in a lot of long-term growing markets, such as: automotive, cloud computing, advanced medical equipment, mobile internet and of course AI.

End Markets (Investor presentation)

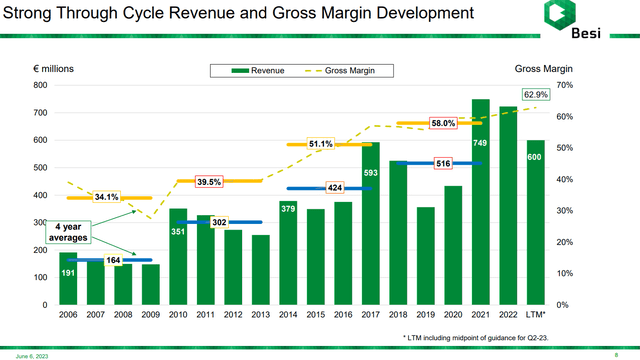

BESIY has managed to grow its revenue significantly every cycle, while also increasing their margins. They even achieved a gross margin of 64% in their latest earnings, which was even higher than expected.

Revenue and Margin development (Investor presentation)

The balance sheet is very healthy with more cash equivalents and deposits compared to its total debt . This is a good sign in a high interest rate environment.

Balance sheet data (2022 annual report )

Also their dividend growth track record is impressive. The company is really shareholder friendly with generous dividends paid and a 10-Year dividend growth CAGR of 36.13%. Just to put some things in perspective, if you bought some shares in November 2013 around €4 euro per share the yield on cost based on the last dividend of €2.85 would be 71%. That’s what I call some serious dividend growth. BESIY has a policy of paying out 40-100% of net income per year in the form of dividends. As a dividend growth investor it is very important to see strong dividend growth and with the current prospects there are no signals this trend will end soon. Choppy dividend growth can still be expected in the future and will be corresponding with the cyclical nature of the company.

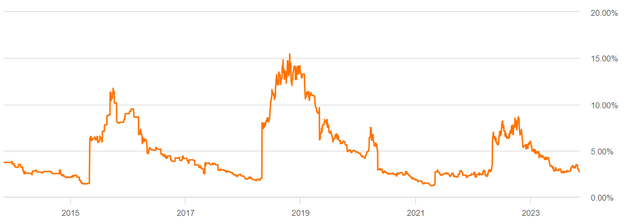

At the moment the dividend yield is 2.58%, which is low compared to its own historical average. Looking at the dividend yield chart it is clear that there were some really nice buying opportunities during the 10-year period.

Dividend yield development (Seeking Alpha)

In 2022 it was possible to buy some shares of BESIY with a dividend yield of 8.65%. In 2018 and 2015 it was even possible to achieve a yield above 10%. The moments that BESIY shares had a high dividend yield were actually good moments to buy shares. And I know that is hard to time the market, but in my opinion it can be valuable to look at the dividend yield to determine if the time is right to buy this stock. Seeing that the dividend yield now is 2.58% is an indication that the stock is on the expensive side.

Q3 2023 earnings report

The latest earnings were received very well by investors. At the day of releasing its earnings report the share price of BESIY went up significantly. The revenue of 123.3 million and net income of 35 million were lower (24.1% and 33.5%) compared to Q2 2023, but it was in line with the expectations. The decline in revenue and net income was the result of the current general market headwinds and the weakness in demand of high-end smartphones.

The main positive was that their orders were 13.1% higher. This was due to increased demand for next-gen AI applications and of course hybrid bonding. Their margins were also better than expected. The company still achieved a gross margin of 64.6% and a net margin of 29.1%.

If we look at the numbers from a cycle point of view we can see that the last 12 months of revenue were 56.5% higher compared to the last cycle of 2019. The operating profit was even better with a 115.4% increase.

As been said earlier there were also some new hybrid bonding orders from 2 customers including one from a leading subcontractor. This subcontractor is really important because they expect higher sales volumes from them in the future.

Outlook

Furthermore, the company expects an increase of 15-25% in revenues vs Q3, due to planned shipments of hybrid bonding and other advanced packaging systems and gross margins should range between 62% and 64%.

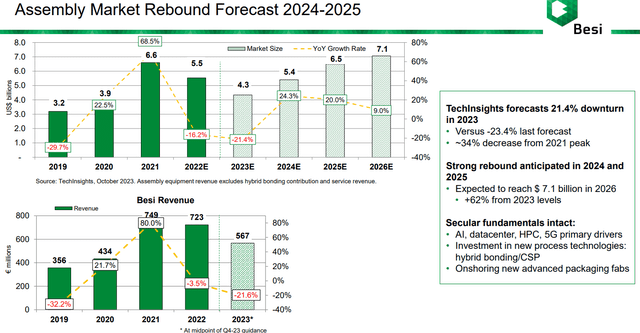

In my view, BESIY’s results are still excellent. Margins remain in good shape despite economic headwinds and they appear to be in an excellent position for the next cycle. With the numbers and the expected outlook in mind things are starting to look better. It is clear that the market is tending to look forward and so is the CEO of BESIY Richard Blickman. He said in the Q3 2023 earnings call that it is likely they’re in the early phase of a new upturn in the assembly market. This implies that we could have seen the bottom of the cycle. There are also other companies that foresee a bottom for the chip market like Taiwan Semiconductor Manufacturing Company (TSM) and Samsung Electronics (OTCPK:SSNLF). TechInsights also forecasts a rebound in 2024-2025.

Market rebound (Investor presentation)

The future of BESIY looks bright and with hybrid bonding in the early adoption phase things will only get better right?

Hybrid bonding

As stated earlier hybrid bonding is the main catalyst of BESIY.

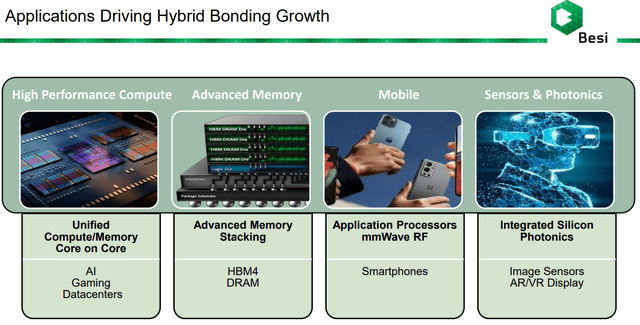

Hybrid bonding is a technique that extends Moore’s Law by 3D system scaling. This technique leads to, greater performance, lower energy costs and more design flexibility.

Hybrid bonding (Investor presentation)

The company states that hybrid bonding has a lot of potential, but it is really hard to tell how large the opportunity will be. A positive sign is that things are getting more concrete.

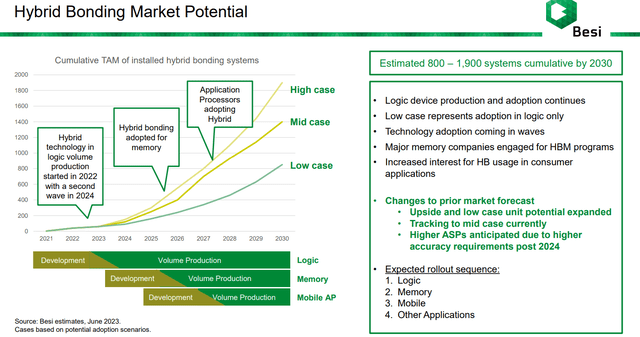

The adoption of hybrid bonding in the chip industry is increasing, even better than they anticipated. For example, Advanced Micro Devices (AMD) has already announced more products that uses the hybrid technique and it looks like that more industry leaders are going to use hybrid bonding as well. What is also good to mention is that BESIY sees an increase in volume in Taiwan and also Intel Corporation (INTC) and SSNLF showed interest in hybrid bonding. In the Q3 2023 earnings call the CEO said that there are at least 40 hybrid bonding systems in the field at the moment. This is just the beginning, BESIY Estimated 800 – 1,900 systems cumulative by 2030.

Hybrid bonding potential (Investor presentation)

So, 2023 and 2024 are all about preparation. They estimated to ship approximately 20 units by the end of the year and it is still uncertain how much it will be in 2024. Costumers don’t give precise numbers in this phase of adoption.

If all things are falling into place, this should lead to significant volume increase in 2025-2026, but it could be also in 2027. This is still in line with the roadmap from their latest capital markets day.

Valuation

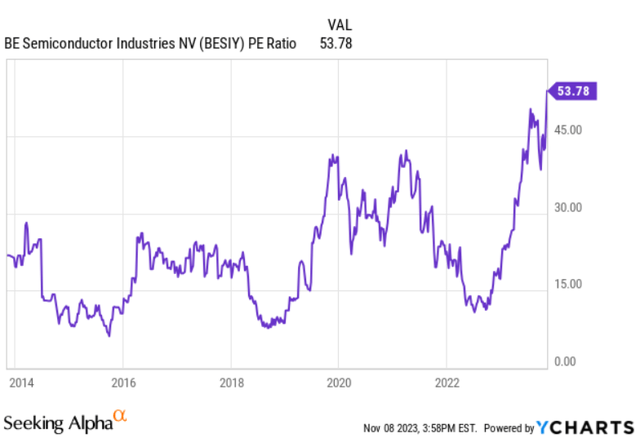

As you can see there are many positives to mention. This is also clearly visible in the valuation of the company. At the moment the PE ratio of BESIY is 53, which can be considered high, also from a 10 year time frame point of view.

PE ratio development (Ycharts)

I don’t necessarily look away when it comes to a high PE. If the company manages to grow its earnings at a rapid pace, the valuation can be justified. Remember that BESIY is a cyclical company, so when earnings growth really picks up the PE ratio can drop quite fast again.

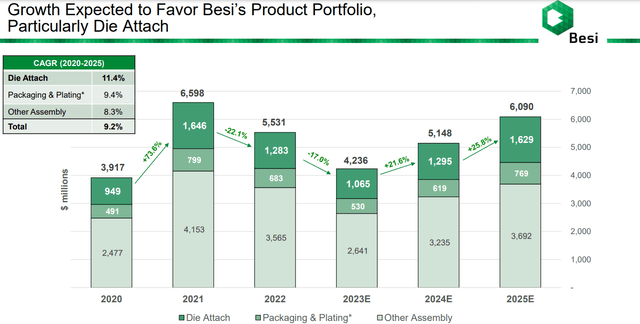

Talking about growth, it is likely that the semiconductor demand will increase. BESIY itself is expecting an average growth of 9.2% CAGR in 2020-2025. This excludes the contribution of hybrid bonding and could potentially be higher.

Product portfolio growth estimates (Investor presentation)

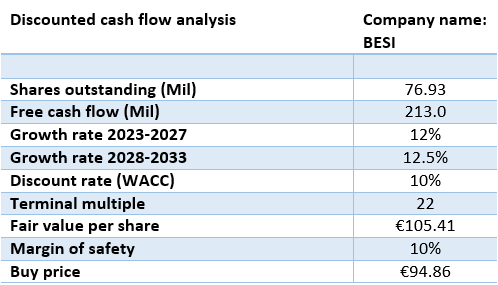

In my last article of BESIY I used discounted cash flow analysis to calculate a fair value of the company. Since BESIY is a company with a very cyclical nature it makes it harder to estimate future earnings growth. For the analysis, a trailing twelve months free cash flow of €213 million was used. I used an average 5-year growth rate of 12% and a 10-year growth rate of 12.5%. The company is expecting an average CAGR of 9.2% of its current product portfolio and some additional growth from hybrid bonding. I expect that the significant contribution of hybrid bonding will start around 2025-2026. After this period I assume the growth will continue.

I used a discount rate of 10%, because I want a return on my investment of at least 10% per year. I used a relatively high terminal multiple of 22, because of the company’s market dominance and high-quality business characteristics. This corresponds to the median PE of 22.4 of the last cycle.

Discounted cash flow analysis (Google spreadsheet)

If we do the math this comes down to a fair value per share of €105.41 . At the moment the share price of BESIY is €110.40. Compared to my own fair value it is 4.73% overvalued.

I am aware that my new fair value is significantly higher compared to my first article about BESIY. In retrospect, I think my old fair value was too conservative. This mainly has to do with the entered free cash flow. I have also adjusted the growth prospects slightly upwards, especially 5-year growth numbers. It would also be a shame to miss out on great (dividend) growth investments by making too conservative assumptions. The growth prospects used could still be too conservative, as the impact of hybrid bonding can be huge. However, there are also some potential investment risks, which will be explained in more detail below.

Investment risks

Before investing in the company it is important to keep some things in mind. BESIY has beta of 1.48 and history shows that the stock price can be quite volatile. Volatility isn’t necessarily a bad thing , but history shows that BESIY can easily drop more than 50% from its peaks. Here are some examples from the past 10 years where the decline was close to or over 50%:

BESIY stock price volatility (Google finance)

There are also some other sector-related risks, which could potentially have quite some impact.

Think about the geopolitical tension in the semiconductor landscape. On the 17th of October the US authorities published an updated version of the advanced computing and semiconductor manufacturing equipment rule. Additional restrictions have been introduced when it comes to export of advanced chip manufacturing technology. This already has impact on companies like ASML and this may also apply to BESIY in the future.

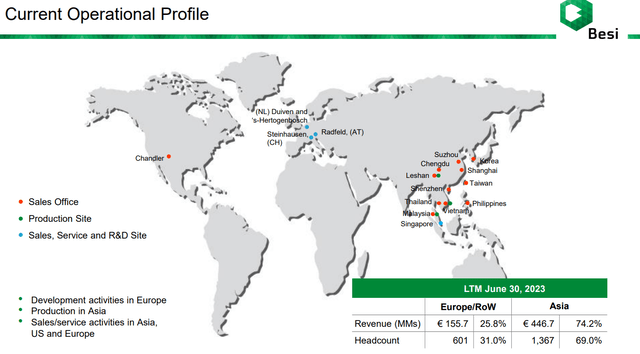

Operational profile (Investor presentation)

Since BESIY is generating a lot of revenue in Asia this can have significant impact on future profits. There is also a possibility that Chinese customers will shift away from European and American companies. A good example from the latest news is Baidu, Inc. (BIDU) that shifts away from NVIDIA Corporation (NVDA) when it comes to their AI chips. This could also happen to BESIY if geopolitical tension increases and/or there is a good Chinese equivalent.

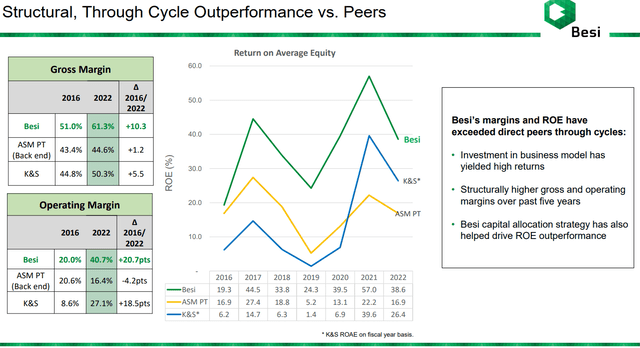

Secondly, there is a possibility that a lot of good news is already priced in. At the moment BESIY is in a great position to profit from hybrid bonding in the future. The company is definitely the one to beat and has a technological edge compared to competition like ASMPT Limited (OTCPK:ASMVY) and Kulicke and Soffa Industries (KLIC).

BESIY vs peers (Investor presentation)

Because the full rollout of hybrid bonding comes later than initially planned, it gives competition time to make their move. On the other hand, BESIY will continue to develop their hybrid bonding machines as well.

Finally, BESIY is a company that has great management with Richard Blickman as a skilled CEO. Blickman is the CEO for a grand total of 28 years, he has a lot of knowledge of the semiconductor landscape and has led BESIY through several business cycles. Given his age, it would be no surprise if he decides to step down from his position in the coming years. When new management takes his place, the question is always whether the current corporate vision will be continued.

Conclusion

BESIY is a high-quality semiconductor equipment company with a top notch balance sheet and excellent dividend metrics. The company can really profit from several megatrends with hybrid bonding as their main catalyst. The company shows that things are starting to fall into place and it will only be a matter of time before BESIY starts generating significant profits from it. Based on discounted cash flow analysis BESIY looks overvalued at the moment. There is uncertainty about the moment when hybrid bonding will make a meaningful contribution to BESIY’s profits. Since there are some geopolitical risks associated with investing in the company it’s good be cautious in making overly optimistic assumptions. Also, the stock is quite volatile and I would advise you to slowly build a position when it hits the fair value price. Based on its high volatility you can also consider to take an extra margin of safety.

I will keep a close eye on the news surrounding BESIY and will also consider slowly expanding my position if the share price drops again. Based on my investment thesis I give BESIY a “HOLD” rating. My personal average buying price is €66 euro per share and it is really hard not to get price anchored. On the other hand, there are plenty of positive aspects to mention why BESIY is a high-quality business and why it can grow its profits significantly in the future resulting in a very attractive dividend growth investment.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

")

")

: A Robust Business Facing A Secular Threat")