")

")

I last covered Trex (NYSE:TREX) back in March where I highlighted some key takeaways from the company’s 2022 annual results. I maintained a previous BUY rating, but will downgrade now to HOLD as shares appear fully priced at current levels.

This isn’t an indication I believe Trex is poised for suboptimal performance. I’m actually quite bullish on Trex headed into 2024, and believe the company is in a far better position than last year at this time.

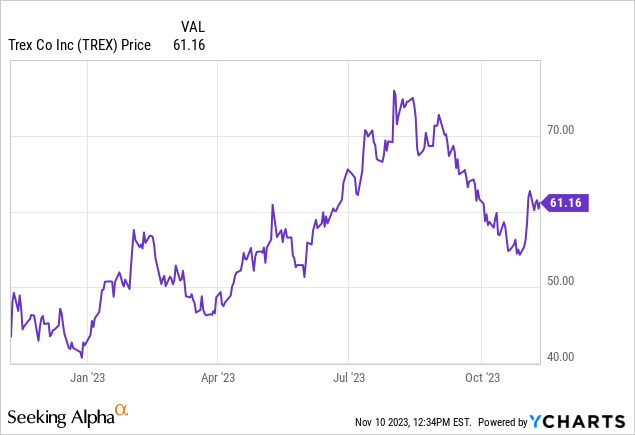

But with a share price north of $60, coupled with Trex’s revenue growth target of 12% through 2028, I can’t make a case for shares to compound +5% above the S&P 500 over the same time period. And if you can’t beat the market, you may as well join in.

Nonetheless, I am excited about some of the new and existing opportunities Trex is leaning into for 2024. I’ll highlight a few here, and will be poised to take up a position if the market decides to re-rate Trex shares in the near future

Leaning Into The Railing Business

Admittedly, prior to listening to Trex’s Q3 2023 earnings call this week, I hadn’t listened to one since Q4 2022. Evidently, a lot has happened at Trex over the past few months because I went from hearing next to nothing about railing to hearing a lot about railing.

Indeed, after Trex sold its commercial products line in late 2022, which mostly installed rod-rail systems, I thought the company wanted out of the railing business. Or that there simply wasn’t enough meat on the bone to warrant continuing operations.

But that seems to have shifted, specifically in the residential space. I’m guessing that through its market research, management identified a meaningful opportunity in railing, and delved into product innovation to see if it could compete with vinyl. Trex was successful, and rolled out its Select T-Rail product in Q2 2023 which is seeing early success.

Here are a few excerpts from Trex CEO Bryan Fairbanks during the Q3 2023 earnings call:

We also see significant growth potential in our broader Residential segment, driven by railing, fasteners, cladding and fencing, which together with decking brings our overall addressable market opportunity to approximately $14 billion. We believe in opportunities in railing alone offer substantial growth potential. The growth will be driven by expanded attachment rates coupled with attractive solutions to match consumer preferences at each price point while still delivering on Trex quality.

And:

While we have manufactured and sold Trex railing products since our early years, we recently accelerated our efforts to further penetrate the market. Notably, we introduced our Trex Select T-Rail system in the second quarter. This composite rail system is priced competitively against low-cost vinyl railing yet outperforms vinyl both in terms of aesthetics and performance. T-Rail is off to a great start, expanding our share in railing and building greater awareness of the Trex brand in this important category. The T-Rail launch continues our strategy of providing railing product at every price point as we have successfully done in decking.

Trex is still primarily a decking company, but it has aspirations to increase attachment rates for railing, which currently ranges wildly by region from 15% to 50%. Attachment rates refers to the percentage of Trex decking customers who also purchase railing. CEO Bryan Fairbanks had this to say during the Q3 2023 call:

But what we do see is where we have those lower attachment rates, that means that there are areas of the marketplace that we’re not hitting the sweet spot for what they’re looking for and they’re all opportunity for us to be able to expand that attachment rate to get it up to 50% to 60% across the board.

10YR Return vs SP500 (Seeking Alpha)

New Product Innovations

On November 9, Trex announced a whole slew of new product innovations. Management hinted around these during the Q3 2023 earnings call, but would not give details. Those details are now here. A few of the highlights include:

- Hardware including fasteners, patented drill bits, depth setters, and plugs

- Trex Signature series to compete at the high-end of the market

- New heat-mitigating technology with the Trex Transcend Lineage line

- Cable and glass railing systems

- Lighted, solar-powered post caps

- And of course, the Trex Select T-Rail system mentioned previously

I believe these new products and innovations have the potential to drive significant growth for Trex over the long term. For the most part, Trex is a company that sells $1 billion in composite decking. But with these new innovations, the company can capture greater share of wallet.

Typically, if you’re installing a deck, you’re going to need fasteners, railing, and lighting. Trex is now giving customers the opportunity to one-stop-shop. This can only be a positive.

When Am I A Buyer?

For me to take up a position, I need to see shares under $50. Trex shares are at $61.10 as of this writing. That means I’m looking for an 18% drop from here.

I doubt the market cooperates with me on this objective. Seeing how the stock is up 12% since announcing earnings on October 30. And management was more optimistic than pessimistic going into 2024, without disclosing too much detail.

But as an investor, you’ve got to stick to your own convictions. Even if it means you “miss” an opportunity. Rest assured, “missing” opportunities will likely save you more than it helps you in the long run.

Conclusion

I’m a big fan of Trex. It’s a great company offering a great product, and is poised to pick up greater share of wallet from its customers. It’s highly profitable, and has generated good returns for shareholders, growing 6x over the past 10 years.

Nonetheless, with shares north of $60, the stock is too expensive. And I have a hard time making a case for it to handily beat the S&P 500 over the next 5+ years.

If you’re an existing shareholder, I say HOLD; you own a solid company. But I wouldn’t recommend taking up a new position unless Trex drops below $50.

Read the full article here

")

")

")

")

")

: A Robust Business Facing A Secular Threat")

")