")

2023 may have begun on a more gloomy note amid the Fed’s rate hikes, but the year is ending with a resurgence in optimism. Yet, most of the 2023 performance has been driven by a small group of stocks (‘the magnificent 7’); this narrow rally means overall market breadth now hovers well below historical averages. Yet, a long-awaited Fed pivot is finally at hand, and this has historically meant strong equity rallies alongside declining real rates. At the same time, overall earnings growth is proving to be very resilient – even after accounting for a lowered consensus bar in anticipation of a macro slowdown next year. So is economic growth, with Q4 Atlanta Fed GDPNow tracking at a very solid ~2.6% pace (off an elevated ~5% Q3 base).

IMG

As the recent outperformance in ‘lower quality’ names showed, a lower rate/resilient growth combination bodes well for the rally broadening out to the tail end of U.S. large-caps. This theme should benefit ETFs tracking a broader large-cap basket. One such fund is the ultra-low-cost Schwab U.S. Large-Cap ETF (NYSEARCA:SCHX), among the broadest US-listed large-cap portfolios at 755 holdings (vs. ~500 for the S&P 500 (SPY)). The fund is also priced lower than SPY at ~22.6x earnings with minimal quality tradeoffs – SCHX boasts a stellar track record of earnings growth (+20.4% over five years) and returns on equity (sustained >20%). U.S. elections later next year and slowing economic activity are risks, albeit transitory ones, that should do little to derail the structural earnings growth story.

Schwab U.S. Large-Cap ETF Overview – Ultra-Low-Cost Exposure to Large-Caps

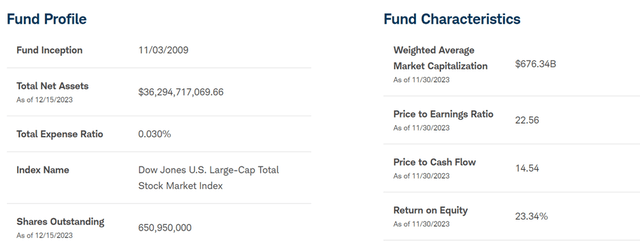

The US-listed Schwab U.S. Large-Cap ETF tracks the total return performance of the market capitalization-weighted Dow Jones U.S. Large-Cap Total Stock Market Index. Unlike other large-cap trackers, SCHX’s size criteria allows it access to stocks with market caps of $70bn (32.2% of the portfolio), expanding its investable universe to over 750 listings – subject to a quarterly rebalancing process. The ETF held ~$36.3bn of net assets at the time of writing and maintains one of the lowest total expense ratios on the market at 0.03%. By comparison, the closest large-cap ETF comparable, Vanguard’s Large-Cap ETF (VV), charges a slightly higher 0.04% despite managing a much smaller 539-stock portfolio.

Schwab

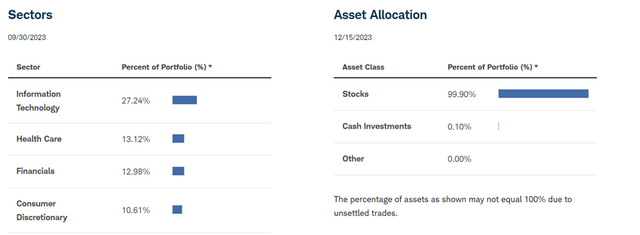

The fund is spread across 755 holdings (including cash), with the largest sector allocation going to Information Technology at 27.2%. Health Care (13.1%) is the second-largest exposure, followed by Financials (13.0%) and Consumer Discretionary (10.6%). Other meaningful sector exposures include Industrials (9.1%), Communication Services (8.6%), and Consumer Staples (6.3%). While the top five sectors account for an outsized ~73% of the total portfolio, SCHX has its sector allocation relatively better spread out than most other large-cap funds. That said, the fund isn’t immune from some volatility, as the 17.7% standard deviation of its returns shows.

Schwab

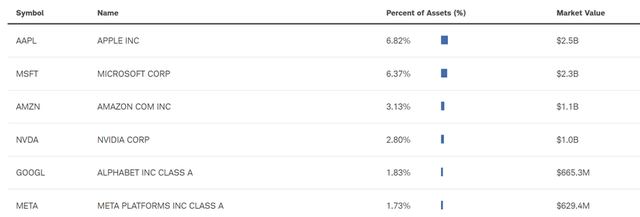

In line with the tech-heavy sector exposure, the fund’s single-stock allocation features a heavy emphasis on tech stocks, with all five of its largest holdings either directly or indirectly involved in tech. Apple (AAPL) is the largest holding at 6.8%, followed by Microsoft (MSFT) at 6.4% and Amazon (AMZN) at 3.1%. Nvidia (NVDA), the biggest gainer this year, is the fourth-largest holding at 2.8%, while Alphabet Class A shares (GOOGL) round up the top five at 1.8%. Tesla (TSLA) and Berkshire Hathaway (BRK) have the largest non-tech allocations at 1.6% and 1.5%, respectively. While SCHX’s portfolio composition is largely in line with most other large-cap funds like VV, its relatively lower single-stock concentration stands out – the result of its portfolio breadth.

Schwab

Schwab U.S. Large-Cap ETF Performance – Steady Outperformer Through the Cycles

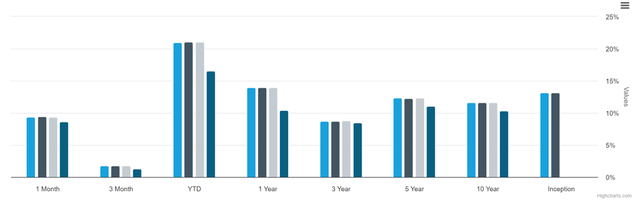

Few equity markets in the world have outperformed U.S. stocks, and SCHX’s annualized +13.2% return since inception (NAV and market price terms) only reinforces this notion. This rang true yet again this year, with SCHX delivering a +21.0% year-to-date total return, only slightly below low-cost S&P 500 trackers like VV. Similarly, over the last five and ten years, the fund has generally kept pace with VV, returning an impressive +12.3% and +11.6%, respectively. Another key plus is the fund’s tracking error, which, to the manager’s credit, has been minimal relative to its benchmark Dow Jones U.S. Large-Cap Total Stock Market Index.

Schwab

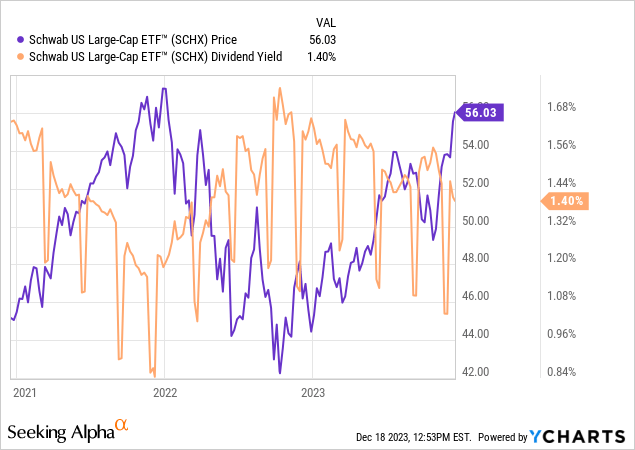

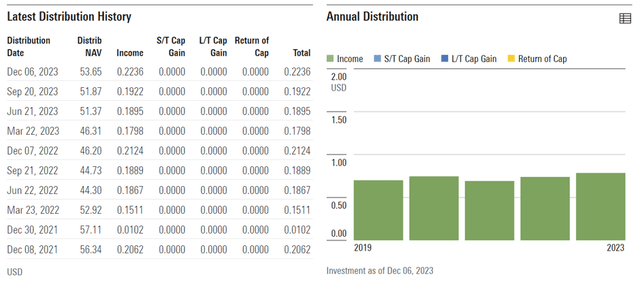

The fund’s relatively lower concentration around high-growth big tech names has kept the distribution yield slightly higher than VV as well, though, at 1.4% (on a 30-day and trailing twelve-month basis), this isn’t the biggest income generator. On the other hand, the fund’s holdings in high-quality companies with some of the most attractive reinvestment runways globally (23.3% portfolio return on equity) make reinvesting excess cash more attractive than distributing to shareholders. Given its quality, growth potential, and declining real rate backdrop, SCHX’s underlying 22.6x P/E valuation doesn’t screen all that richly. And relative to cash flow, SCHX is priced very fairly at 14.5x.

Morningstar

Ride the ‘Everything Rally’ with Minimal Quality Tradeoffs

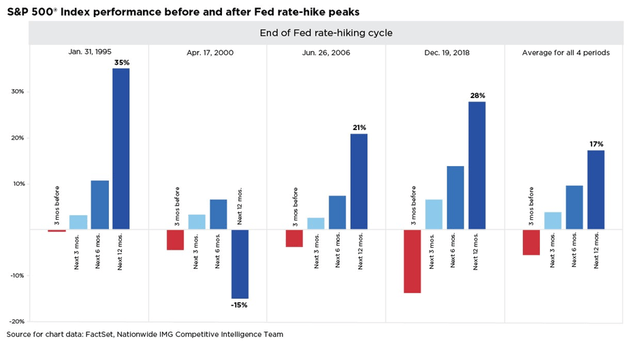

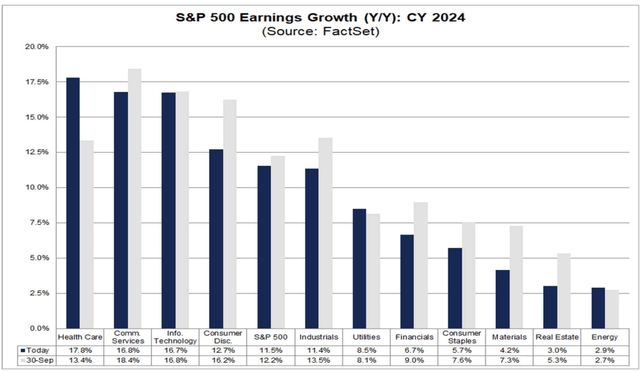

With a Fed’ pivot’ all but certain for 2024, the valuation setup into next year is compelling, given equities tend to rally strongly once a Fed tightening cycle ends. The only catch is earnings, as a ‘hard landing’ scenario could entail further downside to an already lowered consensus bar. Cushioning the impact, though, are tailwinds from fading input cost pressures, as well as the removal of any earnings drags from the cyclical energy and materials sectors, all of which should keep YoY growth positive.

Factset

More earnings growth and sharply declining real rates bode well for the U.S. equity rally broadening out, with the lower-priced tail end of U.S. large-caps poised to benefit this time around (vs. ‘Magnificent 7’ doing the heavy lifting this past year). Net, I favor playing this theme via the lower-priced (but high-quality) SCHX portfolio, one of the broadest baskets of large caps on the market.

Read the full article here

(LFABF) Q4 2024 Earnings Call Transcript")

")

")

")