")

")

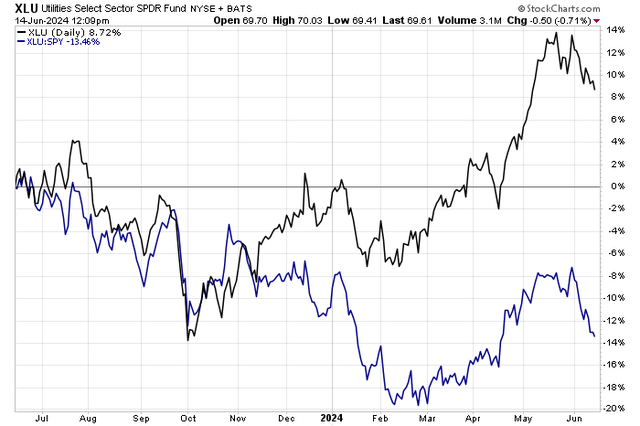

After a powerful burst of absolute and relative strength from the middle of the first quarter through mid-May, the Utilities Select Sector SDPR Fund ETF (XLU) has turned lower and has underperformed the S&P 500. Despite lower interest rates, which usually benefit debt-heavy utility companies, the recent 0.5 percentage point drop in the 10-year Treasury rate has done little to stem a relative downturn in the XLU ETF. Of course, lower yields today in the bond market make one firm’s high yield all the more attractive. Let’s dig in.

I reiterate a hold rating on FirstEnergy (NYSE:FE). I see the Ohio-based utility as near fair value, though the technical situation has improved from what was seen during much of 2023.

The Utilities Rally Loses Steam

StockCharts.com

According to Bank of America Global Research, FE, through its subsidiaries, generates, transmits, and distributes electricity in the United States, and is primarily regulated electric utility conglomerate of transmission and distribution (T&D) assets. The company has more than six million customers across six states (OH, PA, NJ, WV, and MD primarily) with 10 distribution company footprints. FE also owns three transmission utilities regulated by FERC with oversight from state utilities regulators.

Back in April, FirstEnergy reported a decent set of quarterly results. Q1 non-GAAP EPS of $0.55 beat the Wall Street consensus forecast by a penny, while revenue of $3.3 billion was a slight miss. The reported EPS figure was modestly above the mid-point of the company’s guidance. While there was an uptick in degree days, a measure of power demand for a region, and though new rates were a boon, earnings fell on a year-over-year basis. Operational and maintenance costs rose, as did finance expenses.

If we see positive rate-case decisions in FirstEnergy’s coverage area, then there could be upside to the earnings outlook, but weather and natural disasters are a key negative risk, though the latest tornado season seemed to leave FE’s footprint generally unscathed. Given the firm’s elevated debt levels, worsening macro conditions could result in greater equity financing needs, which is a downside risk for the stock.

Looking ahead, FirstEnergy sees FY 2024 EPS in the $2.61 to $2.81 range, with second-quarter per-share profits seen between $0.50 and $0.60. Cash flow and balance sheet issues remain risks for the $22 billion market cap company following litigations over the last several years as well as significant pension obligations.

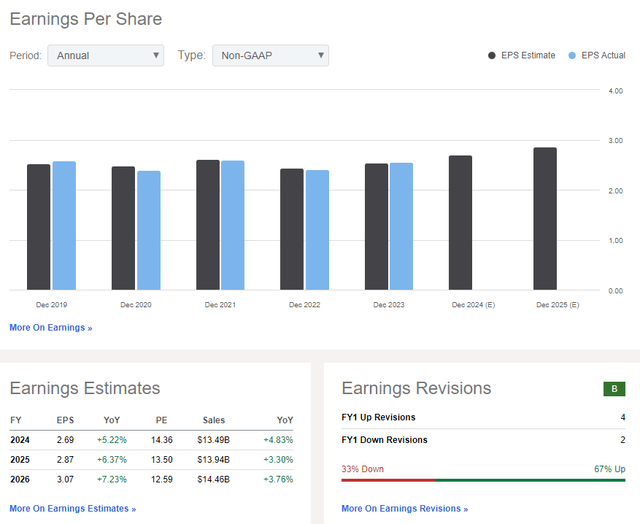

On the earnings outlook, the current consensus forecast calls for $2.69 of operating EPS this year with mid-single-digit growth over the next two years, while revenue is expected to rise at a slightly lower clip. The sellside has turned a bit more upbeat about FE, evidenced by a positive ratio of earnings upgrades to downgrades.

In late May, analysts at Goldman Sachs came out bullish on FE, along with seven other domestic power producers. But bearish news came about two weeks before that when activist investor Carl Icahn exited his stake in FirstEnergy.

FirstEnergy: Earnings Estimates & Sellside Revisions

Seeking Alpha

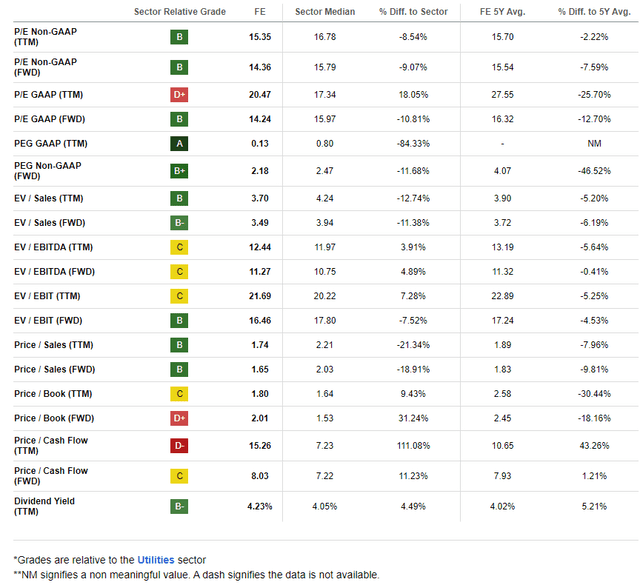

On valuation, we assume $2.75 of non-GAAP EPS over the next 12 months, very close to the consensus forecast, and apply the stock’s 5-year average earnings multiple of 15.5, then shares should trade in the low $40s – close to where the stock is today. If the stock dips just a couple more dollars, it would be good enough to warrant a buy rating.

Considering its high 4.2% trailing 12-month dividend yield, there’s a reasonable valuation case here, but it’s not a compelling deep value, in my view.

FirstEnergy: Valuation Metrics Looking More Favorable, High Yield

Seeking Alpha

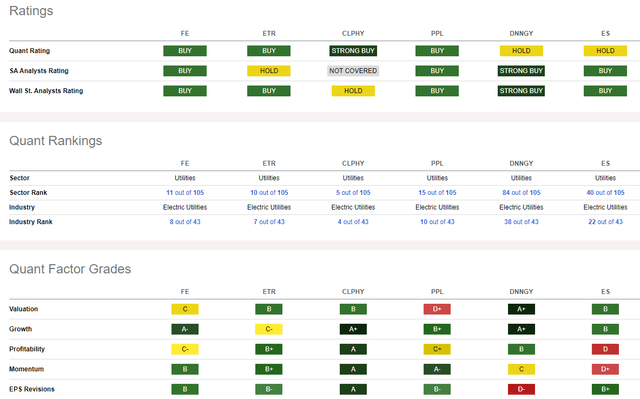

Compared to its peers, FE sports a relatively weak valuation grade, while its growth trajectory is better than many other utilities. But profitability trends and its above-average leverage are indicative of some fundamental weakness. And while the EPS revisions grade is solid, share-price momentum is not overly strong today. I will highlight key trend indicators later in the article.

Competitor Analysis

Seeking Alpha

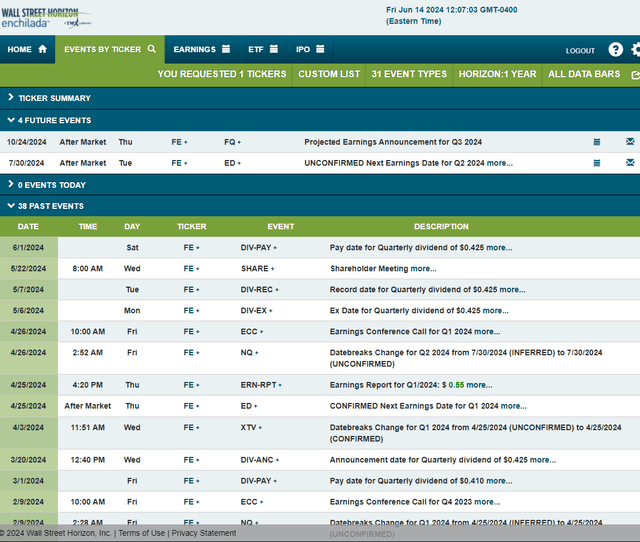

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q2 2024 earnings date of Tuesday, July 30 AMC. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

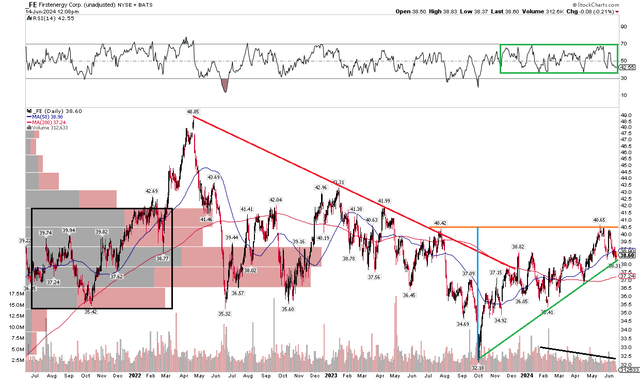

The Technical Take

FE is close to earning a buy rating as far as I see it, but its technical situation remains a significant question mark. Notice in the chart below that shares were able to halt the downtrend that occurred from early 2022 through much of last year, but resistance has emerged between $40 and $41. That’s where sellers have emerged on a pair of occasions in the past 12 months.

What’s encouraging, however, is that there’s now a rising support line that comes into play near the current price point. Moreover, FE’s long-term 200-day moving average appears to be inflecting positive after trending lower for quarters on end. But with a high amount of volume by price up to about $42, we might keep seeing shares churn around current levels.

Overall, FE’s chart is certainly better-looking than it was when I last reviewed the stock, but upside momentum is modest right now.

FE: Shares Attempting A Bullish Reversal, $41 Key Resistance

StockCharts.com

The Bottom Line

I reiterate a hold rating on FE. The valuation is decent, and the yield is attractive, but the stock is just not far enough under what I consider to be fair value. Nor is the technical situation all that bullish as we head into the second half.

Read the full article here

")

")

")

: A Robust Business Facing A Secular Threat")

")

")

")