")

Huge undercount of immigrants since 2022 messes up employment data in the household survey. Census Bureau needs to adopt Congressional Budget Office’s population estimates or go home.

The jobs report data released today is based on two large surveys:

- The survey of “establishments” (employers): nonfarm jobs created (+206,000 in June), various hourly and weekly wage measures, and employment by industry.

- The survey of households: total employment, self-employment, part- and full-time employment, measures of labor force, labor-force participation rates, unemployment, six unemployment rates, employment-population rate, etc.

But the household survey data is wrong because the Bureau of Labor Statistics uses the Census Bureau’s population estimates, but the Census Bureau has so far failed to account for the huge wave of immigrants in 2022 and 2023, according to the Congressional Budget Office (CBO).

CBO came up with its own population estimates by combining data from Immigration and Customs Enforcement (ICE) with Census Bureau data.

CBO estimated that net immigration was 2.67 million immigrants in 2022, and 3.3 million immigrants in 2023, the highest in its data going back to 2000, and about triple the average rate between 2000 and 2021 (1.05 million immigrants per year).

But the Census Bureau has failed to account for the huge influx of immigrants. In terms of population growth:

- CBO: +0.89% for 2022; +1.14% for 2023; highest since 2005.

- Census Bureau: +0.36% for 2022; +0.49% for 2023.

We discussed this at length here, including a chart of the two diverging population growth estimates.

Because the BLS extrapolates its household survey data to the understated population estimates by the Census Bureau, it understates total employment, and understates the labor force, and messes up all other metrics based on them.

So we will no longer cover the household survey data for that reason until Census corrects its population estimates. But we do cover the establishment survey: payroll jobs, wages, and jobs by industry.

The establishment survey: Job growth back to normal, wage growth still higher

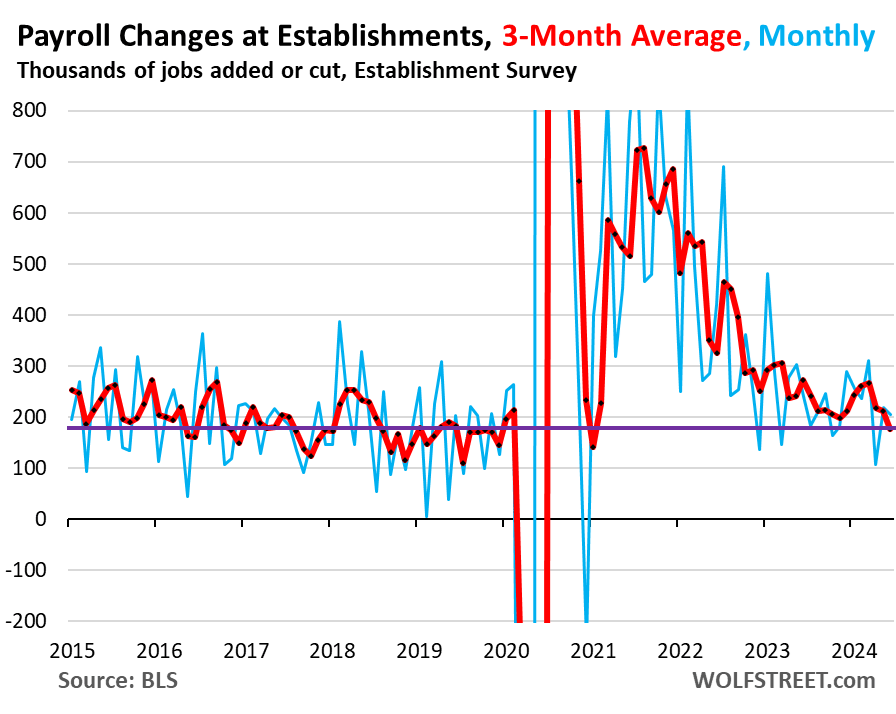

Payrolls at employers increased by 206,000 in June (blue in the chart). Over the past three months, including all revisions, employment increased on average per month by 177,000 (red). This three-month average, which irons out some of the month-to-month squiggles, is right in the middle of job growth in 2017 through 2019, the Good Times (horizontal purple line).

In other words, job growth has slowed from the frenetic pace after the lockdowns and labor shortages, back to the normal pace of the Good Times.

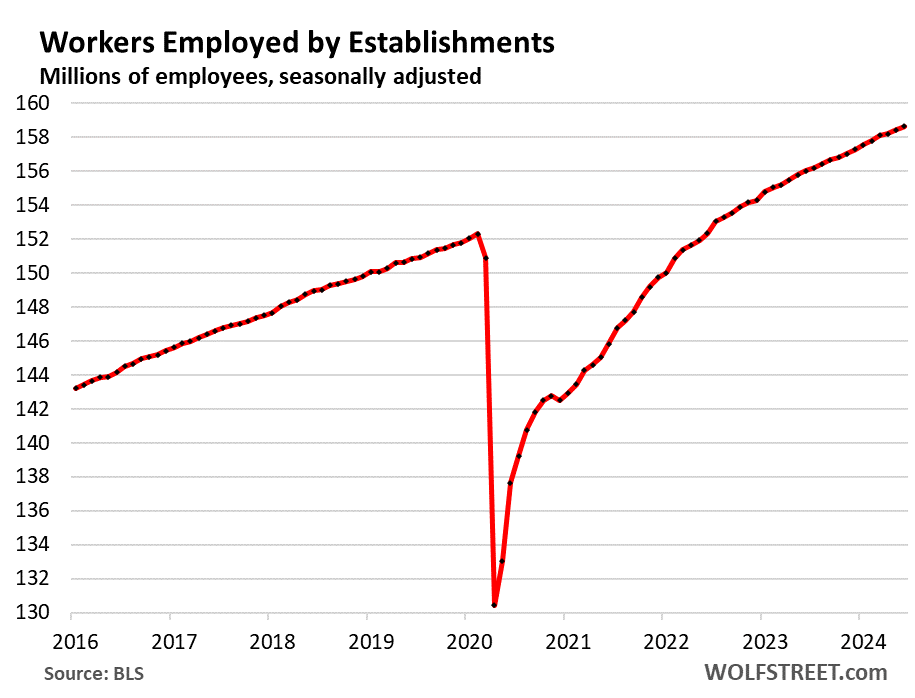

The total number of payroll jobs at employers rose to 158.6 million, a year-over-year increase of 2.61 million jobs (+1.7%).

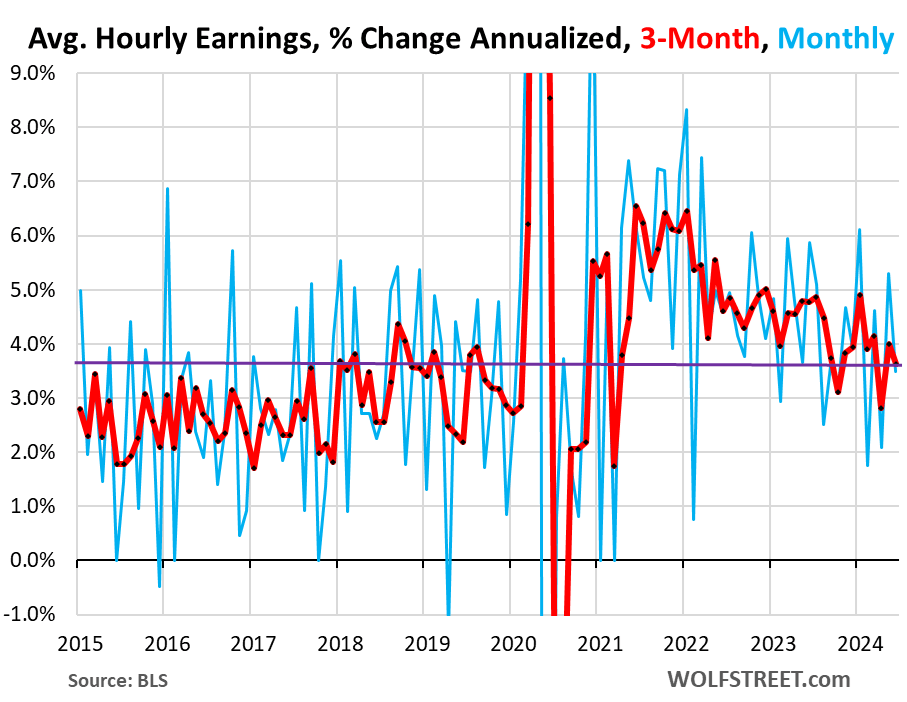

Average hourly earnings increased by 3.5% annualized (0.3% not annualized) in June from May. But May was revised up to an increase of 5.3% annualized, the biggest increase since January, and the second biggest since June 2023.

The three-month average, which includes revisions and irons out some of the month-to-month squiggles, rose by 3.6% annualized.

As we can see in the chart, there was a clear cooling in wage growth from red-hot peak growth at the end of 2021 until October 2023. Since then, there have been a lot of big month-to-month squiggles, but no clear further deceleration of the trend.

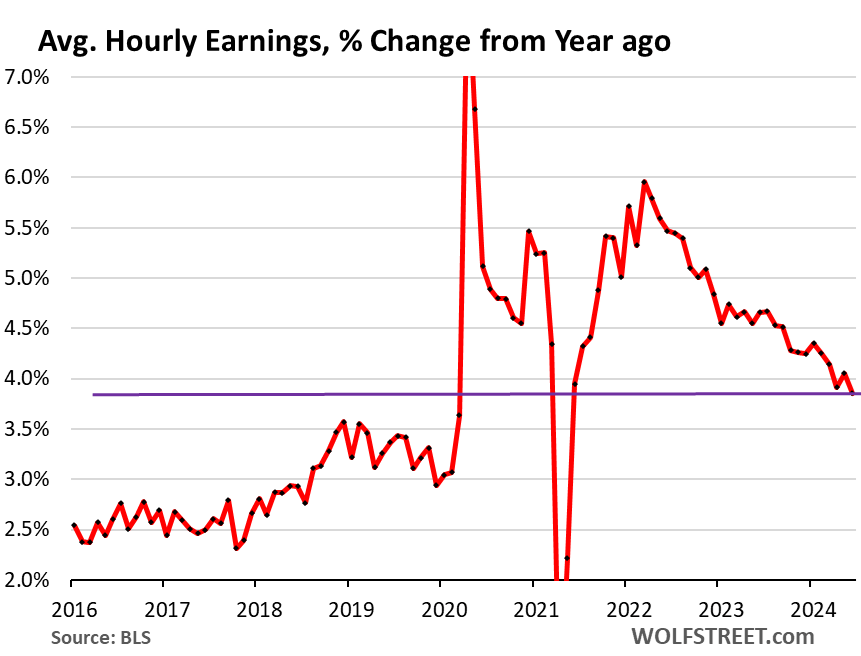

Year-over-year, average hourly earnings rose by 3.9%, and well above the five-year pre-pandemic range of 2.5% to 3.5%:

Longer-Term Trends of Employment by Industry Category

The industry categories are determined by work location. The surveys are sent to employer facilities. The primary activity at that facility determines the industry category. For example, a worker at an Amazon fulfillment center would be under “transportation and warehousing.”

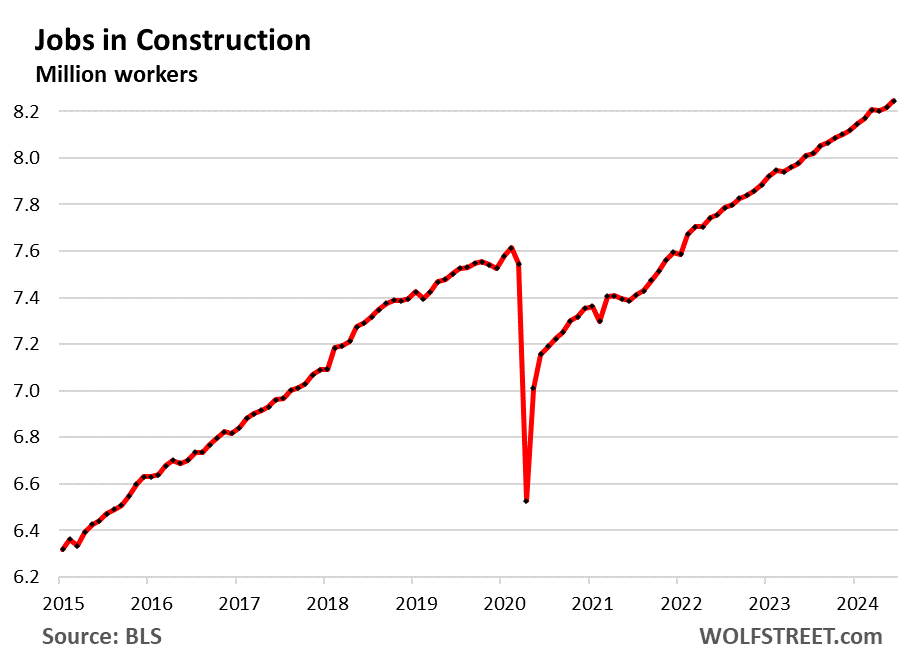

Construction employment (all types, from single-family housing to highways) rose to another record, with tight availability of skilled labor still a problem in some sectors:

- Total employment: 8.25 million, new all-time high

- Month-to-month growth: +27,000

- 3-month growth: +38,000

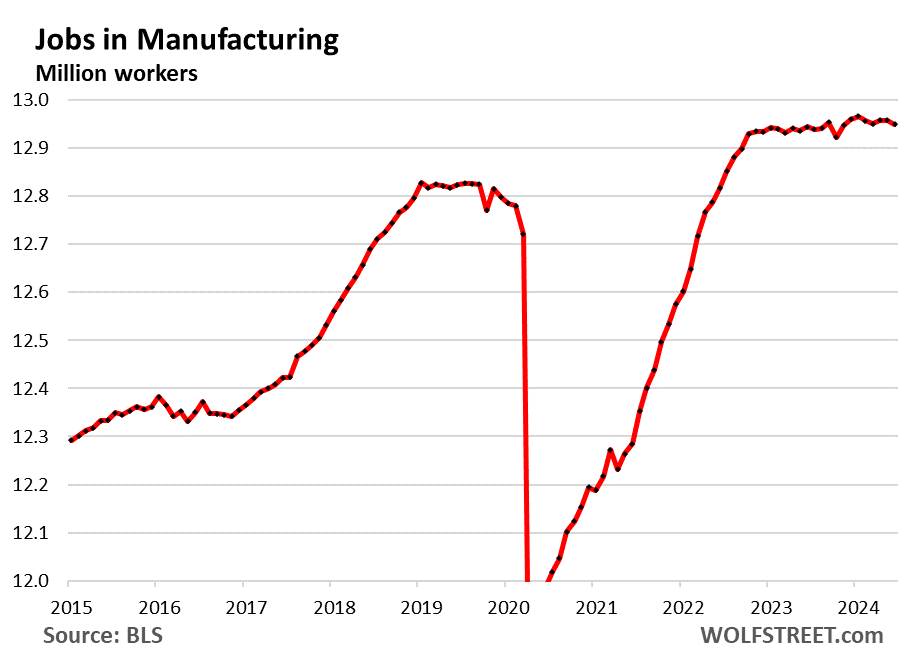

Manufacturing: Employment has plateaued at high levels after a surge out of the pandemic. Automation has ruled for decades, with fewer workers producing more things:

- Total employment: 12.95 million

- Month-to-month growth: -8,000

- 3-month growth: -1,000

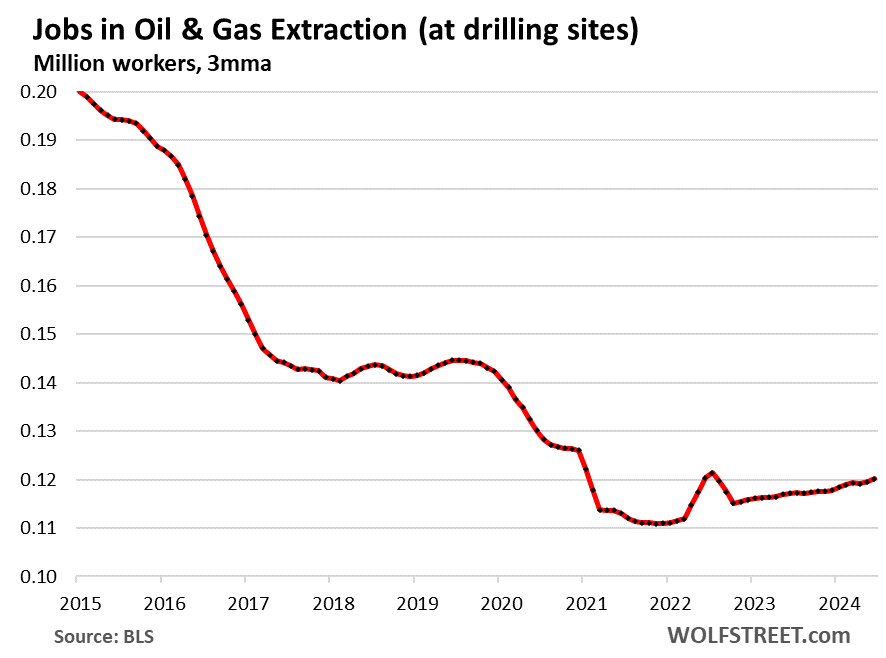

Employment in oil & gas drilling. As a result of the boom in oil and gas production, the US has become the largest crude oil producer in the world and a net exporter of crude oil and petroleum products; and the biggest natural gas producer in the world and the largest LNG exporter. But advanced technologies in the oil and gas field have made production increasingly labor-efficient.

Important: Not included here are the office and lab jobs of oil & gas: tech workers, engineers, traders, finance staff, managers, etc.; they’re counted in other categories, including Professional, business, and scientific services (see further below).

- Total employment: 121,000

- Month-to-month growth: +1,000

- 3-month growth: +2,000

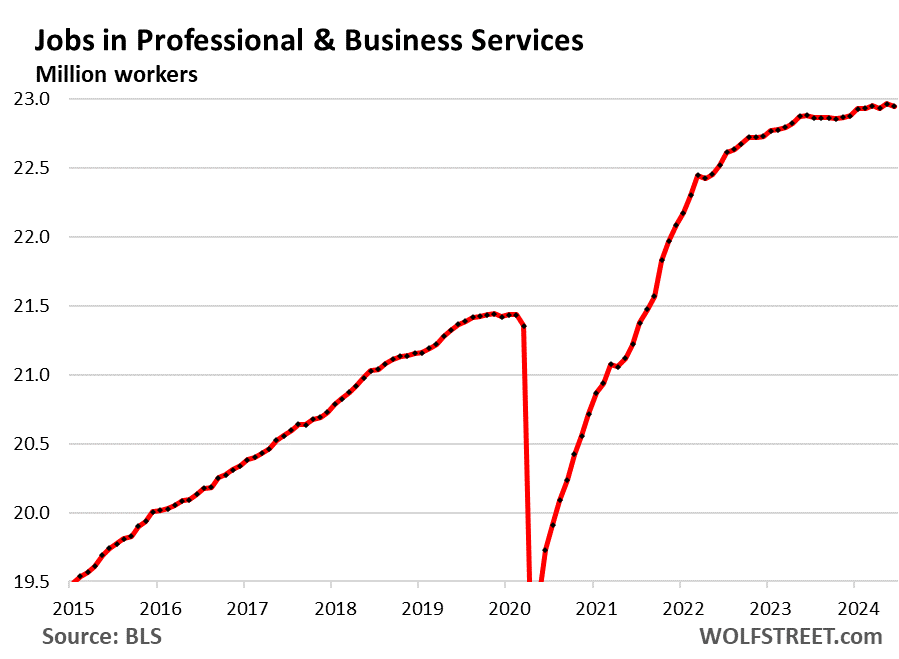

Professional and business services. One of the largest industries by employment, it includes facilities whose employees work in Professional, Scientific, and Technical Services; Management of Companies and Enterprises; Administrative and Support, and Waste Management and Remediation Services. It includes facilities of some tech and social media companies:

- Total employment: 22.95 million

- Month-to-month growth: -17,000 from the record in May

- 3-month growth: -3,000

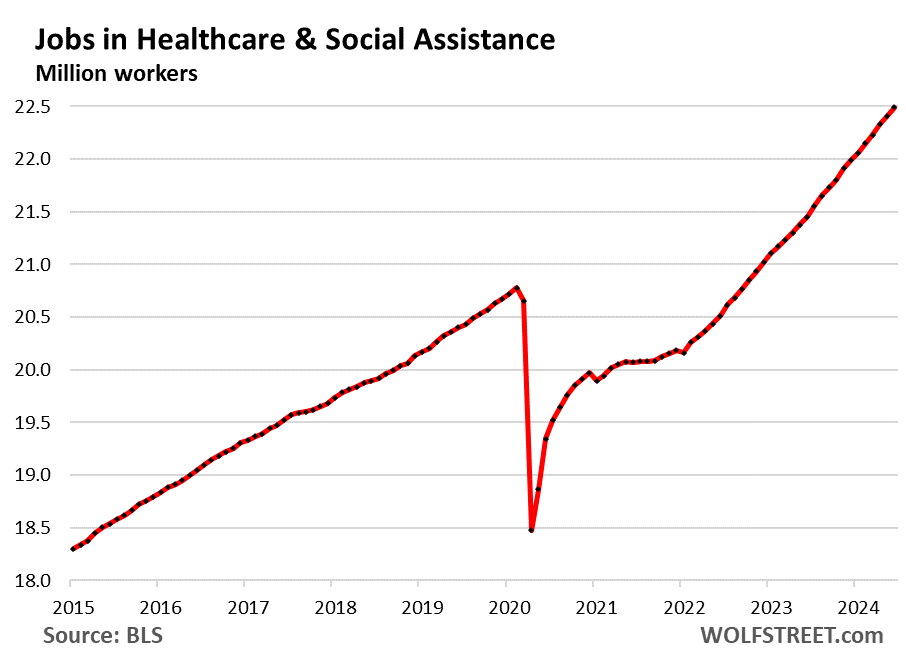

Healthcare and social assistance:

- Total employment: 22.49 million, new high

- Month-to-month growth: +82,000

- 3-month growth: +264,000

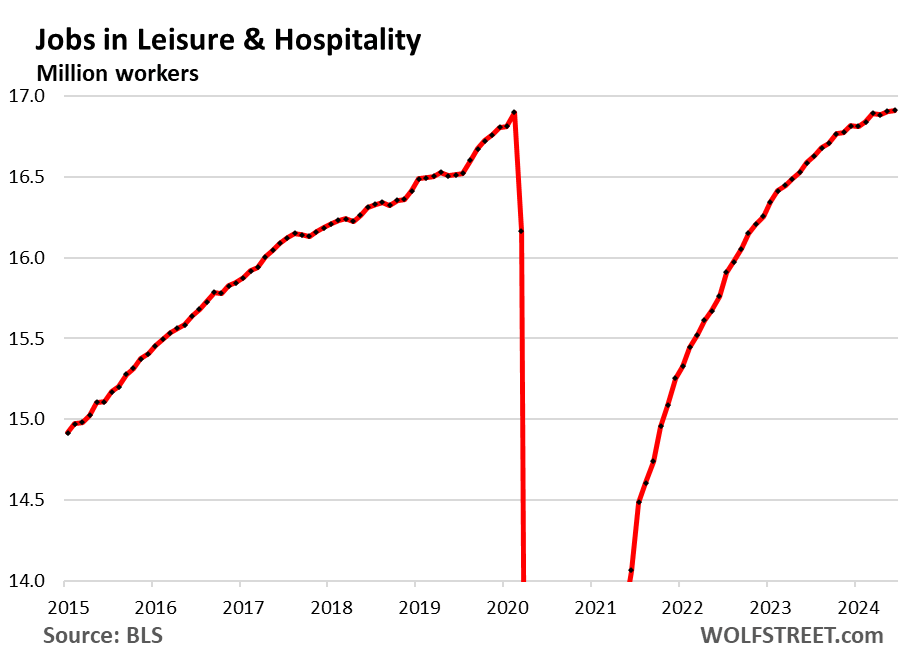

Leisure and hospitality – restaurants, lodging, resorts, etc.

- Total employment: 16.91 million, finally exceeding the pre-pandemic high.

- Month-to-month growth: +7,000

- 3-month growth: +20,000

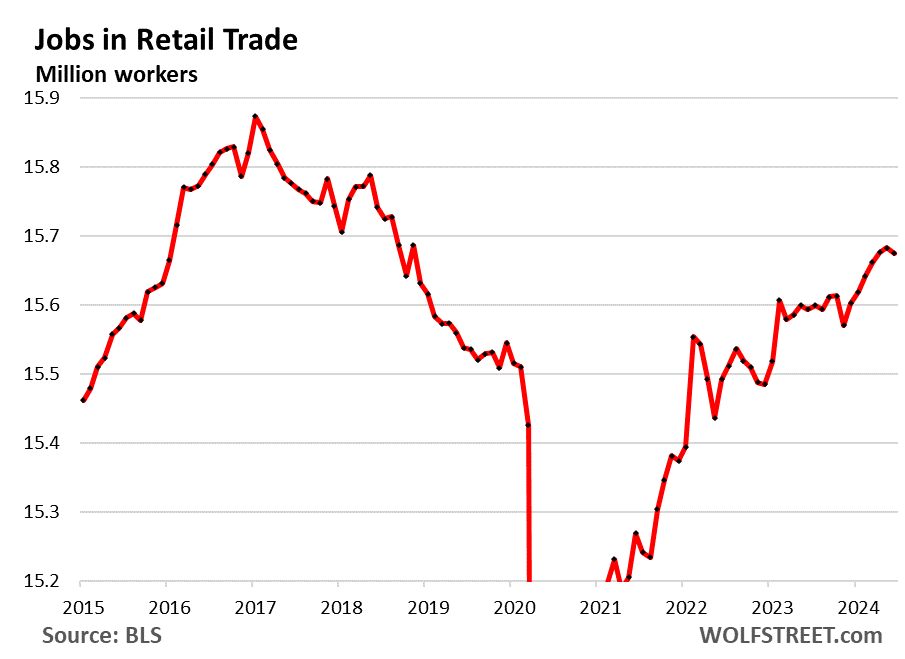

Retail trade counts workers at brick-and-mortar retail stores (at malls, auto dealers, grocery stores, gas stations, etc.). It does not include ecommerce-related tech jobs, drivers, fulfillment-center employees, etc.

A big portion of brick-and-mortar retail has been under heavy pressure from ecommerce for years, with dozens of major retailers being liquidated in bankruptcy court, which we document in our Brick-and-Mortar Meltdown series.

The brick-and-mortar retail sectors that are doing well: those that sell groceries, autos, gasoline, and other stuff that’s hard to buy online. Retailers sell goods. Service providers, such as hair salons, are not considered retailers, but service providers, and employment is captured in other categories.

- Total employment: 15.67 million

- Month-to-month growth: -9,000

- 3-month growth: +13,000

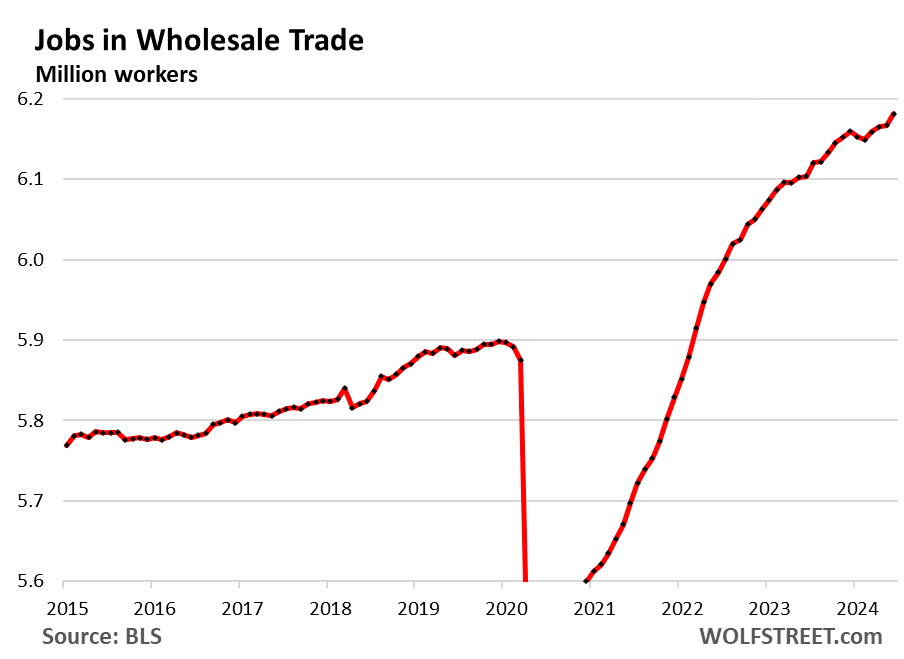

Wholesale Trade:

- Total employment: 6.18 million, new high

- Month-to-month growth: +14,000

- 3-month growth: +22,000

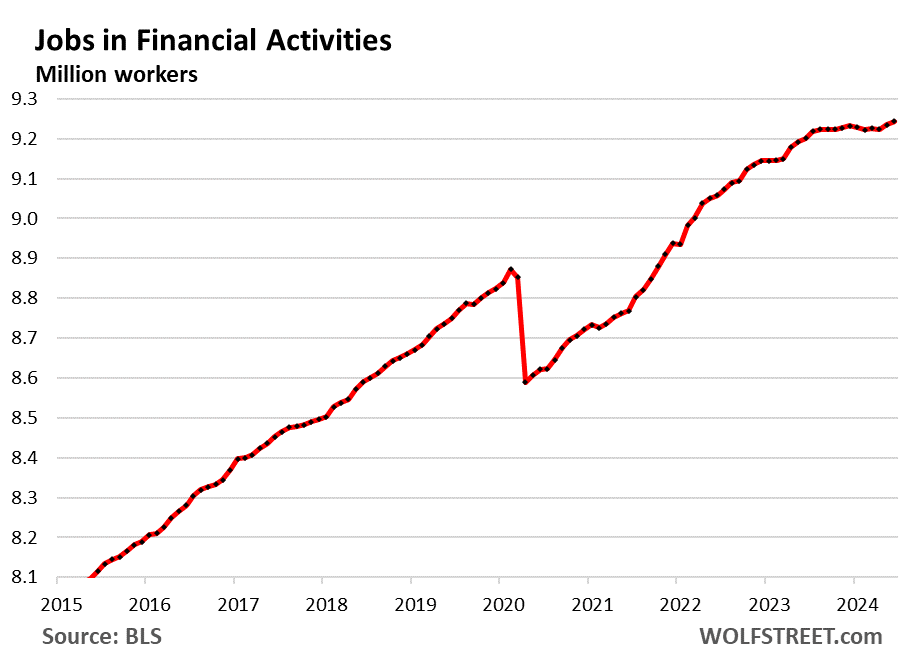

Financial activities (finance and insurance plus real estate renting, leasing, buying, selling, and management):

- Total employment: 9.24 million, new high

- Month-to-month growth: +9,000

- 3-month growth: +18,000

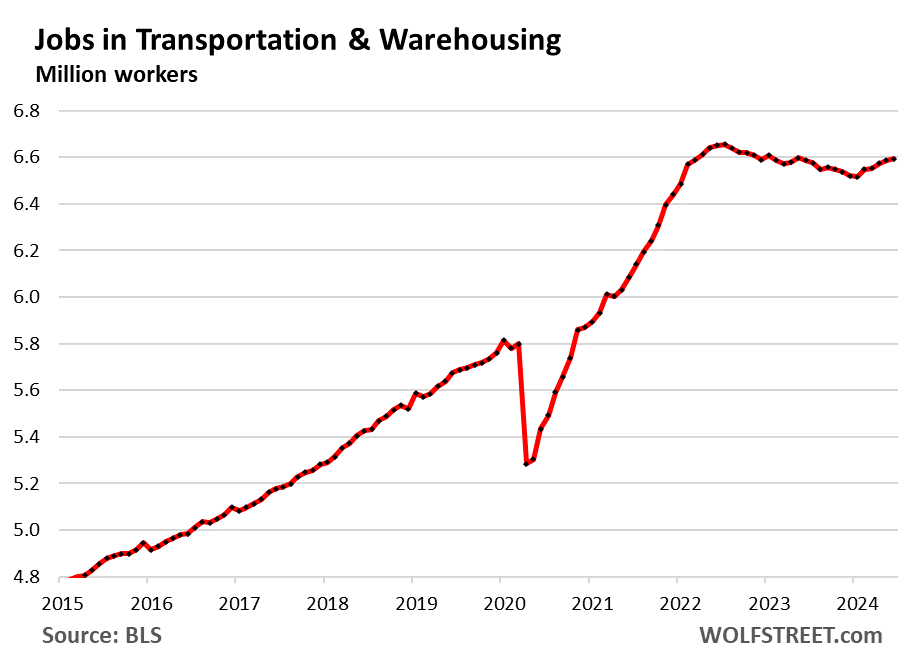

Transportation and Warehousing:

- Total employment: 6.59 million

- Month-to-month growth: +7,000

- 3-month growth: +40,000

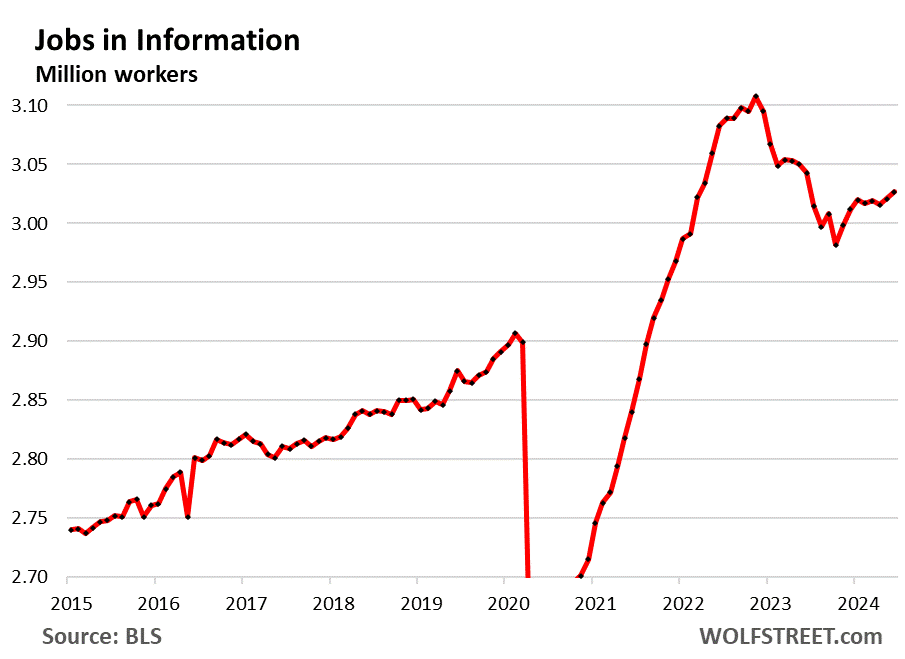

“Information” includes facilities where people primarily work on web search portals, data processing, data transmission, information services, software publishing, motion picture and sound recording, broadcasting including over the Internet, and telecommunications.

This includes some work sites by tech and social media companies. And after the layoffs, they’re hiring again:

- Total employment: 3.03 million

- Month-to-month growth: +6,000

- 3-month growth: +8,000

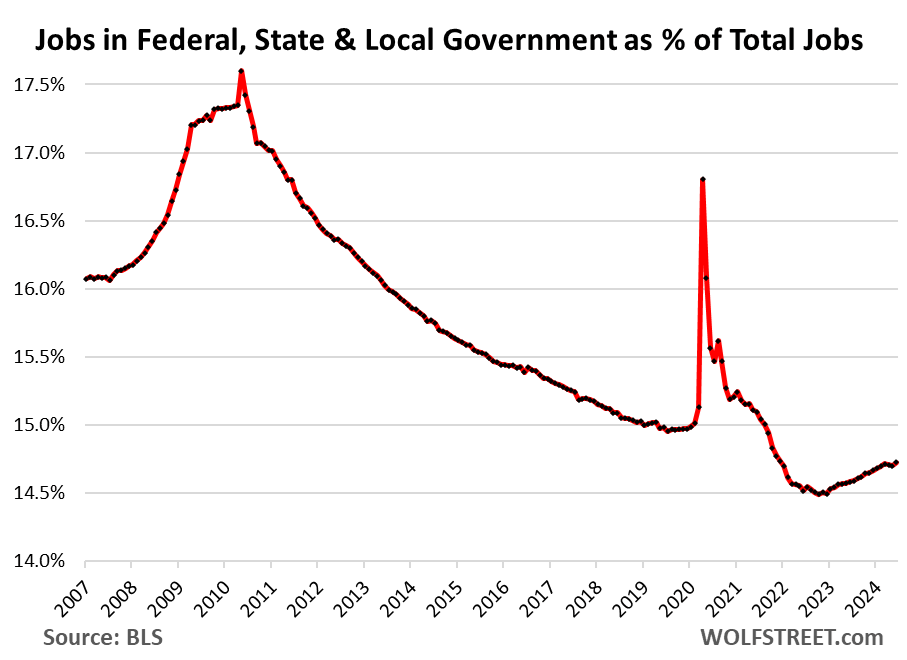

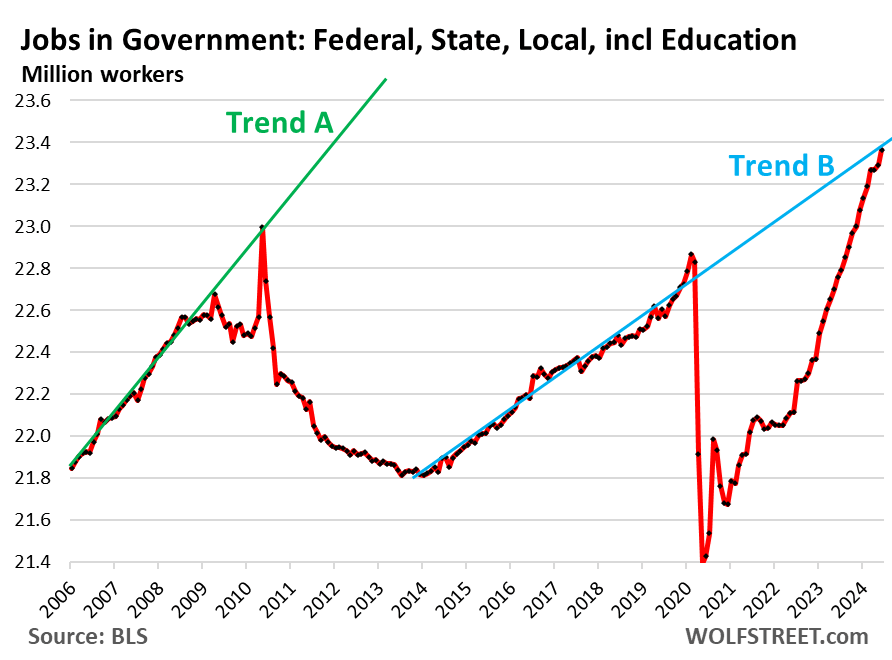

Jobs at federal, state, and local governments:

A historically low 14.7% of all employees work for governments at all levels:

- Federal government: 1.9% of all employees

- State governments: 3.4% of all employees (including higher education, such as at state universities).

- Local governments: 9.4% (much of it in education, such as teachers and school administrators).

The two spikes occurred during census taking (2010 and 2020). The 2020 spike was also a result of the plunge of private-sector employment during the pandemic.

Total civilian employment at all levels of government – local, state, and federal – are now back to Trend B, not Trend A:

- Total employment: 23.36 million

- Month-to-month growth: +70,000

- 3-month growth: +95,000, consisting of +8,000 federal, +21,000 state, +66,000 local, resolving the teacher shortage)

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here

")

")

")

: A Robust Business Facing A Secular Threat")

")

")

")