")

")

Freedom (n.): To ask nothing. To expect nothing. To depend on nothing.”― Ayn Rand.

Today, we put Outset Medical, Inc. (NASDAQ:OM) in the spotlight for the first time. This intriguing medical device/technology concern is trying to transform the dialysis industry. Stocks within the dialysis market had a large selloff this summer on the increasing adoption/rollout of anti-obesity GLP-1 drugs like Ozempic by Novo Nordisk A/S (NVO). Management also brought down its Q3 revenue guidance significant in early October.

In addition, the company received an FDA warning letter in July of this year, which was part of the subsequent guidance cut in October as the rollout of the TabloCart from the market had to be excluded to obtain 510(k) marketing clearance. Management said it has now addressed those concerns and that an interactive FDA review is underway. Is there more pain ahead for shareholders, or is OM stock now in oversold territory? An analysis follows below.

Seeking Alpha

Company Overview:

This medical technology company is based in San Jose, CA. The company provides the Tablo Hemodialysis System, which comprises a compact console with integrated water purification, on-demand dialysate production, and software and connectivity capabilities for dialysis care in acute and home settings. Currently the shares trade just north of six bucks a share and sport an approximate market capitalization of $285 million.

August Company Presentation

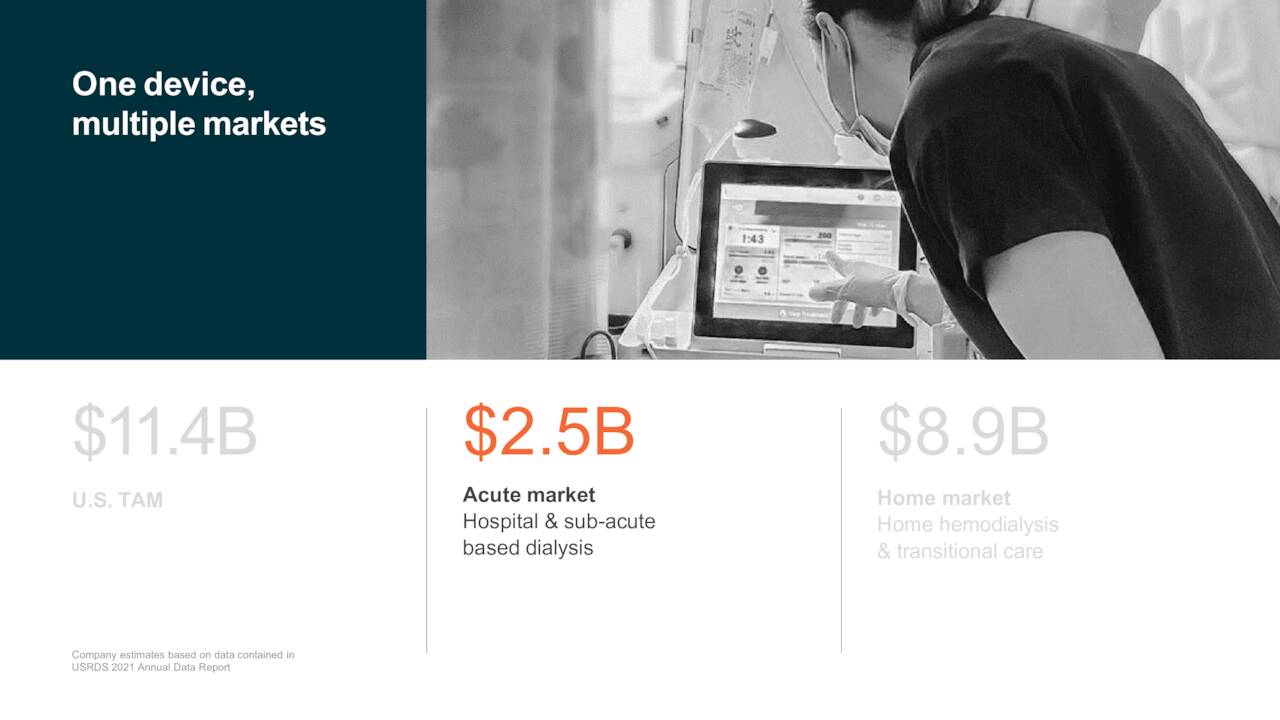

The company’s focus is on “pioneering a first-of-its-kind technology to reduce the cost and complexity of dialysis.” Its Tablo system is aiming at an over $11 billion market.

August Company Presentation

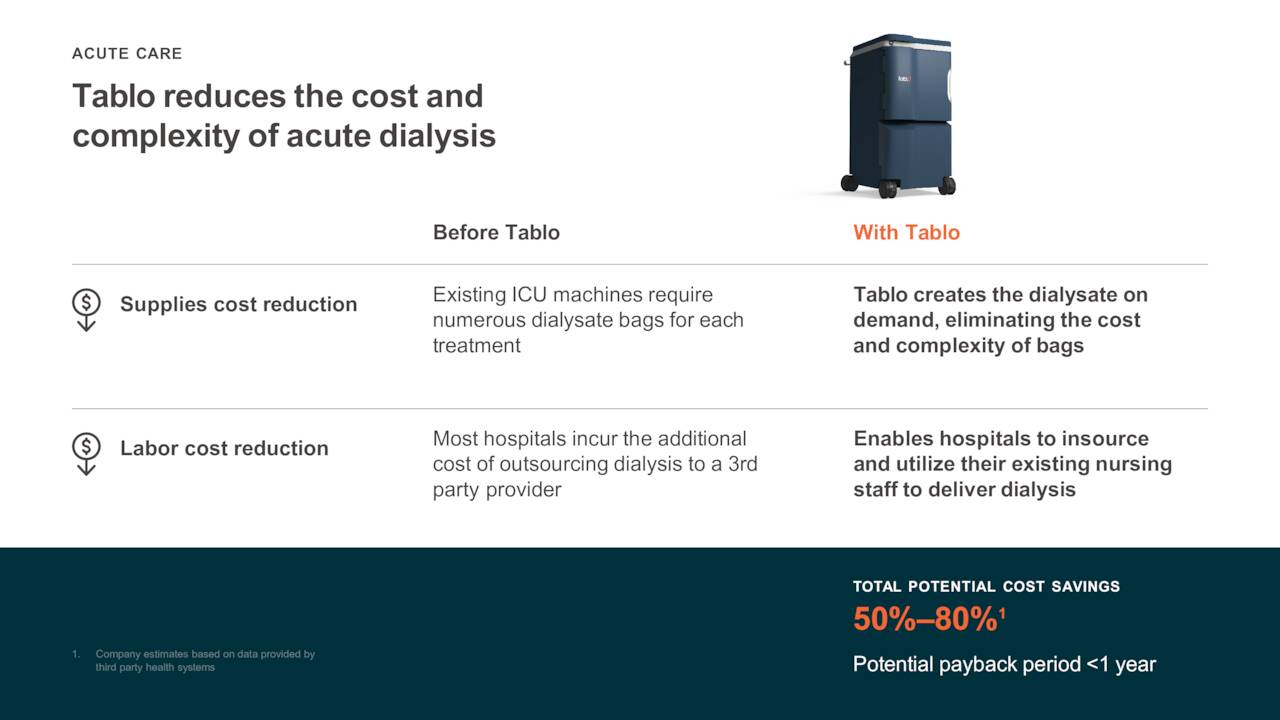

This all-in-one system offers significant cost and supply cost reductions. The company is positioning the Tablo system for both the home and acute dialysis market. The system is now utilized in more than 650 acute and post-acute facilities. Some facilities have noted a 50% reduction in their treatment cost per hour while also reducing the length of stay of their patients in the ICU.

August Company Presentation

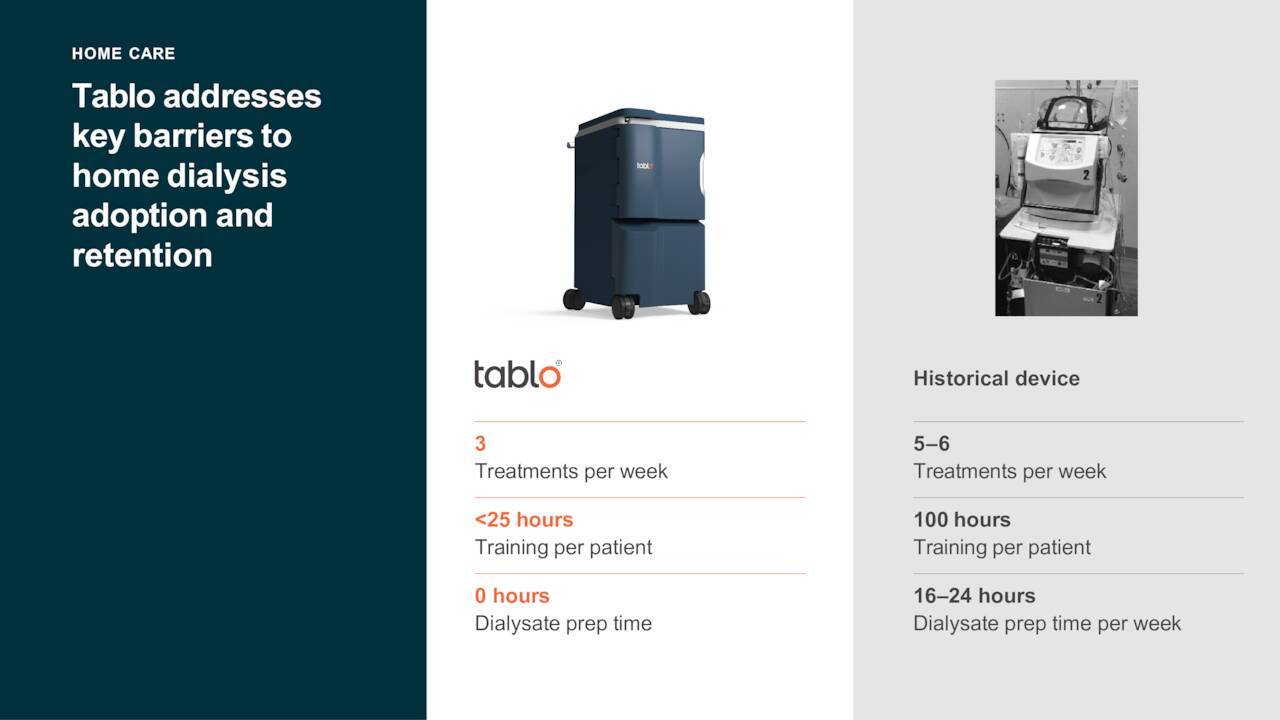

The ease of use and reduced training time has significant appeal in the home setting. The annual cost of the Tablo systems runs about $15,000 annually in a home setting and $20,000 in an acute setting.

Third Quarter Results:

Outset Medical posted its Q3 numbers on November 7th. The quarter saw a non-GAAP loss of 71 cents a share, four cents below the consensus. Sales rose just over nine percent on a year-over-year basis to $30.4, which was in line to expectations. Management reaffirmed its previous guidance for FY2023 revenue of $130 million.

The company expects some 1,400 new Tablo systems to be placed in 2023. Roughly two thirds will be in acute settings while the rest will be home placed. This will leave the company with some 5,400 installed systems by year end.

Analyst Commentary & Balance Sheet:

The analyst community has mixed views around Outset Medical currently. Since third quarter results posted, both RBC Capital ($14 price target) and TD Cowen ($9 price target) have reissued Buy ratings on the stock. Bank of America ($3 price target) has reiterated its Sell rating, while Morgan Stanley ($5.50 price target, up from $5 previously), has maintained its Hold rating on OM.

Just over 15% of outstanding float in the shares is currently held short. Several insiders have been consistent and frequent sellers of the shares throughout 2023. However, sales have ebbed since the stock plunged over the summer. Insiders have disposed of just over $50,000 worth of equity collectively so far in the fourth quarter.

Outset Medical ended the third quarter with $197 million worth of cash and marketable securities on its balance sheet after posting a GAAP Net loss of $46.2 million for the third quarter. On a non-GAAP basis, Outset Medical had a net loss of $35.3 million. Net losses by either measure were slightly above those of Q3 2022, it should be noted. Outset Medical has negligible debt. Management expects to end FY2023 with some $160 million worth of cash on its balance sheet.

Verdict:

Outset Medical lost $3.38 a share on just over $115 million in sales in FY2022. The current analyst firm consensus has losses dropping to $2.74 a share in FY2023 on $130 million of revenues followed by a loss of $2.07 a share in FY2024 as revenues rise by 15%.

The company technology seems like it could be “best of breed” in the dialysis market. However, it is unknown to what extent the new GLP-1 drugs could impact the dialysis market over time. Overall sales growth has slowed significantly from what was projected earlier in the year. Analyst firms also seem to have mixed views on the company’s current prospects.

More importantly, Outset Medical, Inc. is bleeding cash at a prodigious pace, and at its current quarterly burn rate, is likely to going to need to raise additional capital at some point in 2024. Therefore, while I find the Tablo system intriguing, I am passing on any investment recommendation around Outset Medical at this time.

To find yourself, think for yourself.”― Socrates.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

: A Robust Business Facing A Secular Threat")

")

")