")

")

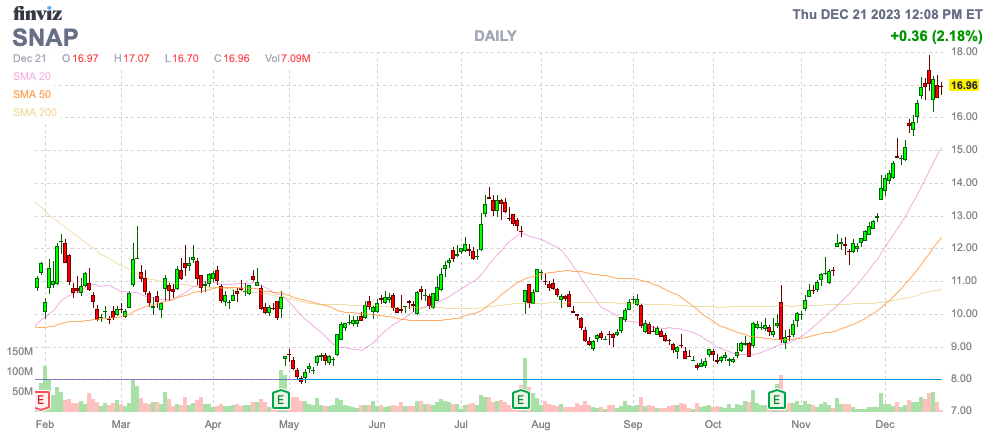

Snap Inc. (NYSE:SNAP) shares have doubled in the last quarter, and the stock likely has much more upside. A lot of small and mid-cap stocks were crushed during the last couple of years, providing substantial upside to just return to more normal valuations. My investment thesis remains Bullish on the social messaging stock, though investors clearly missed an opportunity to own Snap at far lower levels.

Source: Finviz

7 Million Reasons To Own

Only months after I repeated a call to load up on Snap below $9 due to the promising Snapchat+ subscription growth, the company came out and astounded the market with additional subscriber growth. As of early December, Snapchat+ now has 7 million subs.

The subscription service, offering exclusive artificial intelligence (“AI”) features, amongst other functions, to users, has seen explosive growth this year. At $3.99 per month, Snap already generates $28 million per month and $336 million annually now in recurring revenues.

In addition, Snap CEO Evan Spiegel highlighted big 2024 forecasts for the business, adding to the excitement around the stock. The company set what appeared an aggressive target for Snapchat+ subs along with other targets as follows:

Grow Community and Engagement

- 475+ Million Daily Active Users in Q4 ’24

- Grow Content Viewers to 80% of DAU

- Grow Content View Time per Viewer +15% in the U.S. and Globally

Grow Revenue and Earnings

- +20% YoY Full Year Ads Revenue Growth

- 14 Million Snapchat+ Subscribers by EoY and $500 million in non-Ads Revenue

- $500 million of Adj. EBITDA and Positive Free Cash Flow.

Lead in Augmented Reality

- Grow Lens Unique Users to 75% of DAU

- Grow Lens Actions (Save, Post, Send, or Play >6s) +10% per User

- Leverage Generative AI to Transform Lenses and Content Creation.

The Snapchat+ target of 14 million subs by EoY 2024 already appears more plausible with the company hitting 7 million subs in just December. Snap even set a goal of $500 million in no-ads revenue, and this goal appears an easy hurdle now.

Our previous research highlighted how Snap subscription revenues will soar over time based on sub growth and the potential to hike prices. Netflix (NFLX) offers a prime example of how subscription prices can climb over time.

In the case of Snap, a jump to 10 million subs early in the year along with a price hike to $5/month would allow Snapchat+ to generate $50 million in monthly revenue. The management team has a goal for $500 million in non-ads revenue in 2024, but the company could start generating subscription revenues at a $600 million annual rate in early Spring.

The stock market will be much more focused on the run rate with the 14 million Snapchat+ sub. target. With the price hike to $5/month, Snap could exit 2024 with a subscription business generating $840 million in revenues, though the company hasn’t made any indications that price hikes are part of the plan.

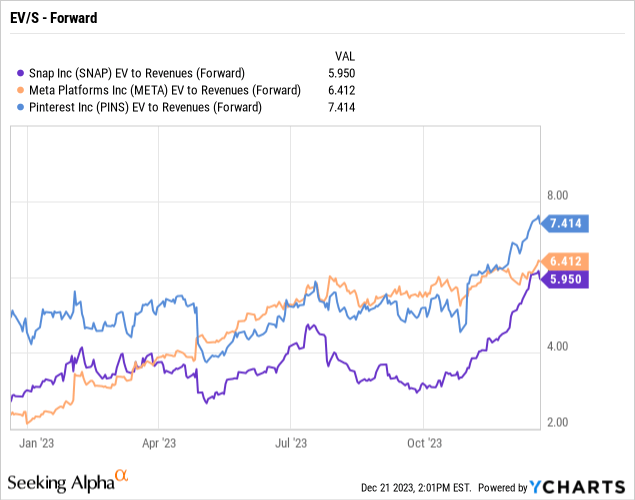

Only $27 Billion

Even after this major rally, Snap is only worth $27 billion. The stock has only regained the social media group multiple with a forward EV/S multiple of 6x. Meta Platforms (META) and Pinterest (PINS) both trade closer to an average of 7x sales estimates now.

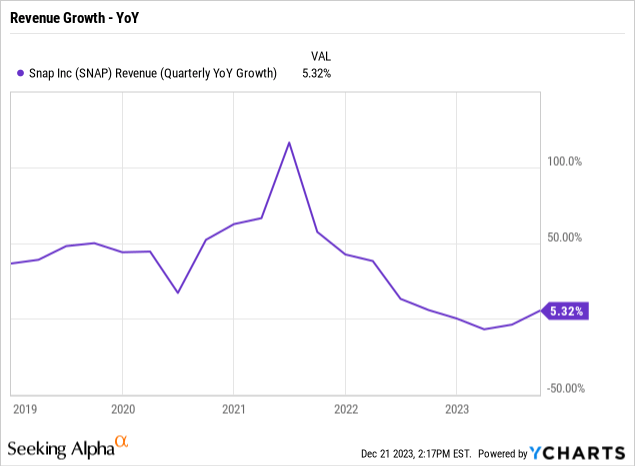

Guggenheim recently forecast Snap sees ad revenues rebound in 2024. The social messaging company already has an ads business with up to $4.5 billion in targeted revenue for 2023.

The consensus revenue targets for 2024 of $5.2 billion would mostly factor in the growth from the subscription business. The analysts target has a 13% revenue growth rate for the year, but the additional revenue amount is only $600 million.

Snap has a history of volatile ad revenue growth with periods of consistent growth followed by over 100% growth in 2021 after the Covid slump. If anything, the company has been hit by a period of digestion after massive growth, while Meta only topped 50% growth in one quarter and overcame the Apple (AAPL) ID issues quicker.

Meta is now forecast to maintain consistent revenue growth in the 10% to 15% range, with a revenue base reaching $150 billion next year. Snap has shown a propensity of growing far in excess of the growth rates of Meta during good times, and one should invest assuming faster growth rates return, considering the boost from subscription revenues requires the need for only limited ad revenue growth to smash current estimates.

Snap has forecast ad revenues to grow by 20% in 2024. Were the company to hit that goal with subscription revenues soaring, the company could easily reach 30% growth for the year.

Snap could see revenues approaching $6 billion in 2024, while analysts are down at only $5.2 billion. The social messaging company doesn’t need to hit this upside potential to reward shareholders, but the stock will be far higher in a scenario where this occurs.

Takeaway

The key investor takeaway is that Snap Inc. remains an appealing stock, even after doubling off our previous call. The company is poised for upside revenue surprises in 2024, and stocks usually react favorably to such situations.

Read the full article here

")

")

")

")

: A Robust Business Facing A Secular Threat")

")

")