Phinia Inc. (NYSE:PHIN) recently reported lower EPS GAAP than expected, and the company is a recent spinoff. However, I do not see why the company could trade at close to 4x EBITDA. I also believe that further improvements of the commercial vehicle market and potential adoption of hydrogen solutions could bring significant free cash flow (“FCF”) growth and net sales growth. Besides, the stock repurchase program could enhance the demand for PHIN stock. Despite the risks from recent restructuring efforts, changes in the environmental regulation, or the relationship with the previous owner of PHIN, I think that the stock is much undervalued.

Phinia, A Recent Spinoff That Increased Its 2023 Guidance

Phinia develops, designs, and manufactures integrated components and systems that contribute to optimize performance, increase efficiency, and reduce emissions in combustion for commercial vehicles and other industrial applications.

Source: Company’s Website

The company is a recently formed spinoff from a large and established corporation. Many investors may not know the know-how accumulated in the past inside a larger organization.

On December 6, 2022, BorgWarner Inc. (BWA) announced plans for the complete legal and structural separation of BorgWarner’s Fuel Systems and Aftermarket businesses from BorgWarner by the spin-off of its wholly-owned subsidiary, PHINIA, which was formed on February 9, 2023. On July 3, 2023, BorgWarner completed the Spin-Off in a transaction intended to qualify as tax-free to the Company’s stockholders for U.S. federal income tax purposes. Source: 10-Q.

Source: SA

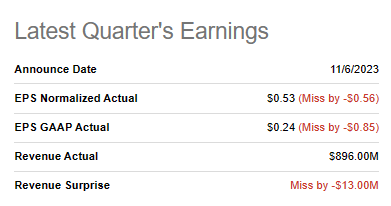

The recent quarterly earnings release, which was lower than expected, may also explain the current valuation. In the last quarterly report, Phinia Inc. noted lower quarterly revenue than expected as well as EPS GAAP lower than expected. Quarterly revenue stood at close to $896 million, and EPS was close to $0.24 per share.

Source: SA

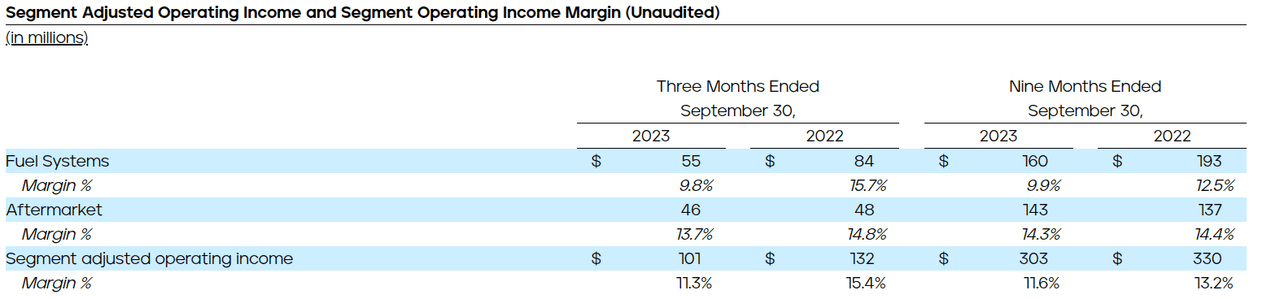

I also dislike the fact that in the nine months ended September 30, 2023, fuel systems margin decreased to about 9.9%. Clearly, the operating margin is lower right now than what it was in 2022.

Source: 10-Q

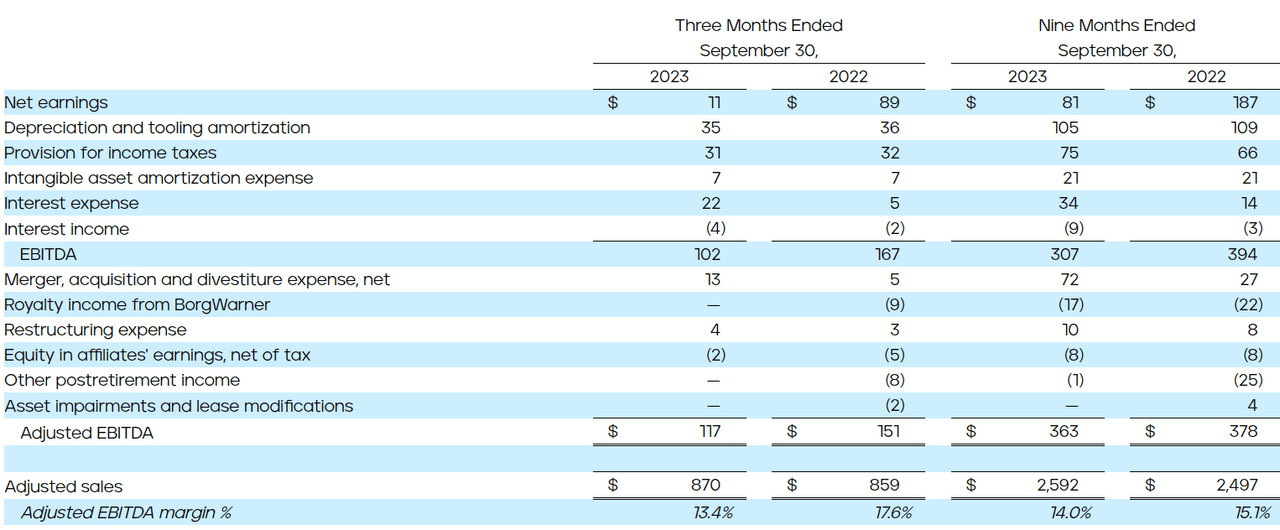

In the nine months ended September 30, 2023, the adjusted EBITDA margin decreased to close to 14%. It was close to 15.1% in the same period in 2022. The company noted that certain contract manufacturing agreements with former parent and higher supplier-related, and inflationary costs were responsible for the decline in profitability.

Cost of sales increased $26 million related to certain contract manufacturing agreements with Former Parent that were entered into in connection with the Spin-Off. Source: 10-Q Cost of sales was also impacted by higher supplier-related and inflationary costs of approximately $23 million arising primarily from $17 million non-contractual commercial negotiations with the Company’s suppliers and normal contractual supplier commodity pass-through arrangements. This impact was partially offset by $7 million of net supply chain savings initiatives. Source: Source: 10-Q

In the nine months ended September 30, 2023, Phinia Inc. reported Adjusted EBITDA of $363 million, which could imply total EBITDA of close to $484 million. Currently trading with a total enterprise value of $1.8 billion, I believe that the current EV/EBITDA is not far from 4x. Given this figure, I would say that Phinia does not look expensive.

Source: 10-Q

It is also worth noting that the company recently increased its guidance for 2023, which I believe could enhance the total valuation soon. 2023 Adjusted sales are expected to be close to $3.40 billion to $3.45 billion, with adjusted EBITDA of $465 million to $475 million.

With commercial vehicle sales running lower than expected in China with key customers, impact from strikes in North America and less favorable currency than expected, the company is revising its FY 2023 outlook for net sales of $3.44 billion to $3.50 billion, adjusted sales of $3.40 billion to $3.45 billion, adjusted EBITDA of $465 million to $475 million, and adjusted EBITDA margins of 13.6% to 13.9%. Expected full year 2023 tax rate is also revised to 34%. Source: PHINIA – PHINIA Reports Solid Third Quarter 2023 Results.

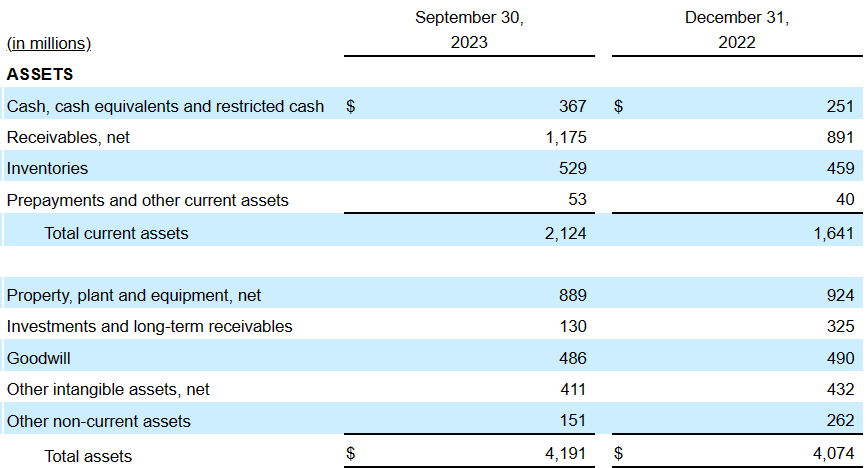

Balance Sheet

With a significant amount of cash in hand, Phinia receives payments from clients a bit late, so management uses some debt financing to function. The total amount of property and equipment is larger than the total amount of long term debt, so I am not really worried about the total amount of debt.

As of September 30, 2023, management reported cash, cash equivalents, and restricted cash worth $367 million, with receivables of about $1.175 billion and inventories worth $529 million. Total current assets stand at about $2.124 billion, and the current ratio is larger than 1x, so I believe that liquidity does not seem a problem here.

Additionally, with property, plant, and equipment of close to $889 million, investments and long-term receivables of $130 million, and goodwill close to $486 million, total assets stand at $4191 million. The asset/liability ratio is close to 2x, so I would say that the balance sheet remains quite stable.

Source: 10-Q

Short-term borrowings stand at close to $87 million, with accounts payable worth $817 million, total current liabilities of about $1.321 billion, retirement-related liabilities of $ 94 million, and long-term debt of $713 million. Finally, total liabilities were equal to $2.299 billion.

Source: 10-Q

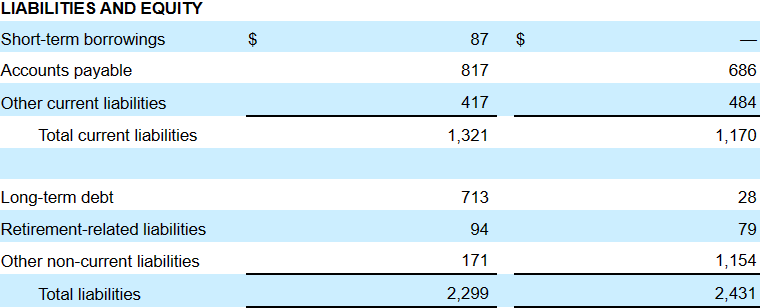

Debt Outstanding And Cost Of Capital Assumed In My Financial Model

In the last quarterly report, Phinia Inc. noted debt agreements and loans, which included interest rates close to 5% and linked to EURIBOR and SONIA. With this information, I believe that a cost of capital of close to 3% and 9% would make sense.

Source: 10-Q

The following lines offer information with regard to the Term Loan A Facility and Term Loan B Facility that Phinia included in the last quarterly report. Note that the EURIBOR stands currently at close to 3%-4%, however it may change in the near future.

An interest rate equal to (1) solely in the case of U.S. dollar-denominated loans, adjusted term SOFR, (2) solely in the case of euro-denominated loans, Euro Interbank Offered Rate (“EURIBOR”), or (3) solely in the case of pound sterling-denominated loans, adjusted Sterling Overnight Index Average Reference Rate (“SONIA”) (which includes a 0.0326% credit spread adjustment to SONIA), as applicable, in each case for the applicable interest period plus a rate with respect to adjusted term SOFR for the Revolving Facility and the Term Loan A Facility, EURIBOR and SONIA, ranging from 2.50% to 3.00% depending on our consolidated net leverage ratio, and with respect to adjusted term SOFR for the Term Loan B Facility, 4.00%. Additionally, the Company will pay a quarterly commitment fee based on the actual daily amount of the available Revolving Facility commitment. Source: 10-Q

I Believe That New Product Development, Recovery Of The Commercial Vehicle Market Could Enhance Future Business Growth

Given the current balance sheet, I believe that we could expect further development of new products, which may enhance future net sales growth. In this regard, management offered the following optimistic expectations and positive long-term outlook.

The Company maintains a positive long-term outlook for its global business and is committed to new product development and strategic investments to enhance its product leadership strategy. Source: 10-Q.

It is also worth noting that further improvement of the commercial vehicle market and adoption of hydrogen solutions could enhance the Phinia FCF line. Additionally, I believe that public support to initiatives that lower global emissions may also enhance the company’s net sales growth.

There are several trends that are driving the Company’s long-term growth that management expects to continue, including recovery of the commercial vehicle market, increased overall vehicle parc driving that supports aftermarket demand, adoption of product offerings with hydrogen solutions for combustion vehicles to serve as a viable alternative to electrification or fuel cell solutions and increasingly stringent global emissions standards that support demand for the Company’s products driving efficiency and reduced emissions. Source: 10-Q.

I Assumed That Restructuring Expenses Would Not Endanger Future Business Opportunities

According to the most recent quarterly report, Phinia Inc. appears to be executing restructuring efforts and evaluating other options to reduce structural costs. Under my financial model, I assumed that PHINIA Inc. would successfully reduce operating expenses in the coming years, and lower headcount growth may not affect operating performance.

Restructuring expense was $4 million and $3 million for the three months ended September 30, 2023 and 2022, respectively, related to individually approved restructuring actions that primarily related to reductions in headcount. The Company continues to evaluate different options across its operations to reduce existing structural costs. As we continue to assess our performance and the needs of our business, additional restructuring could be required and may have a significant cost. Source: 10-Q.

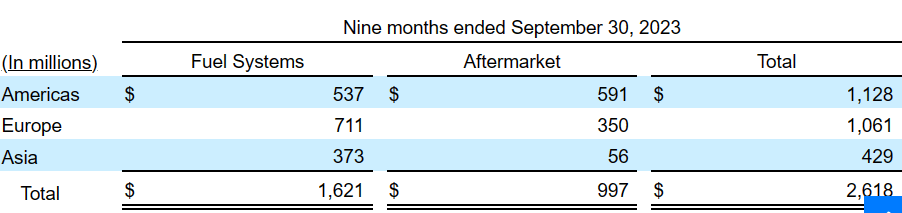

Exposure To Markets In Asia, Americas, And Europe Will Most Likely Help Reduce Total Net Sales Volatility

Phinia reports a significant amount of sales in the Americas, Europe, and Asia. As a result, I believe that the company may offer lower net sales volatility than peers that operate in more niche markets, or exhibit geographic concentration. It is also worth noting that the company offers a significant amount of exposure to the euro currency as Europe appears to be the most relevant market. Investors believing that the EUR/USD may increase in the near future may like Phinia Inc.

Source: 10-Q

Valuation In The Sector, And My Valuation Estimates Using My Previous Assumptions

For the exit multiples, I took a look at the valuation reported by peers. According to Seeking Alpha, the sector median EV/ Forward EBITDA stands at close to 10x. It is significantly higher than the current valuation reported by Phinia Inc. Peers appear to be trading a bit more expensively than PHIN. Given this figure, I assumed that an exit multiple between 5x and 8x would make sense.

Source: SA

Source: SA

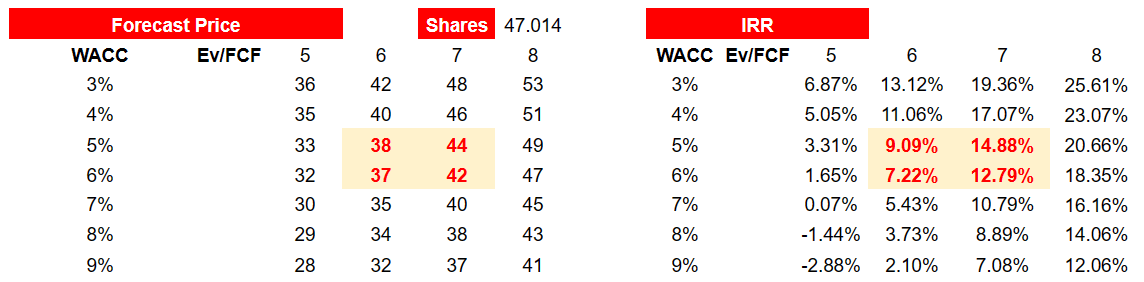

My valuation figures include 2027 net earnings worth $266 million, with depreciation and tooling amortization close to $183 million, intangible asset amortization of $36 million, and stock-based compensation expense of about $12 million.

Additionally, with changes in receivables of about -$215 million, changes in inventories of close to -$105 million, and changes in accounts payable and other current liabilities of close to $295 million, I obtained 2027 net cash provided by operating activities of about $453 million. Finally, if we include 2027 capital expenditures, including tooling outlays of about -$168 million, 2027 FCF would be $299 million.

Source: Oren’s Expectations

With FCF close to $95 and $299 million, a WACC of 3%-9%, and an EV/FCF between 5x and 8x, I obtained an enterprise value close to $1.7 billion and $2.9 billion. Besides, if we add cash and subtract debt, the implied equity valuation would be between $1.2 billion and $2.5 billion with a median equity of $1.7-$2.05 billion.

Source: Oren’s Expectations

Dividing by the current share count, the median implied fair price would be $37.1-$44.2 per share, and we would be talking about an IRR of about 7% and 15%.

Source: Oren’s Expectations

Risks

Phinia Inc. reports certain ties with BorgWarner, which some investors may not appreciate. Additionally, BorgWarner may decide not to provide services to Phinia Inc., or increase its prices. As a result, I believe that Phinia Inc. may see a decrease in its FCF margins, and the stock valuation could decline.

These services do not include every service that we have received from BorgWarner in the past, and BorgWarner is only obligated to provide the transition services for limited periods following completion of the Spin-Off. Following the Spin-Off and the cessation of any transition services agreements, we will need to provide internally, or obtain from unaffiliated third parties, the services we will no longer receive from BorgWarner. Source: 10-Q.

I also dislike that Phinia Inc. reports accounts payable due to BorgWarner. In the future, if management is forced to pay much faster, increases in working capital could lead to new debts, which may lower the stock valuation of Phinia Inc.

In the Condensed Consolidated Balance Sheets, the Company presents $186 million within Accounts payable and $99 million within Other current liabilities. These amounts were previously presented as Due to BorgWarner, current. In addition, the Company presents $957 within Other non-current liabilities as of December 31, 2022. These amounts were previously presented as Due to BorgWarner, non-current. Source: 10-Q

Finally, I think that the company could suffer significantly from volatility in the price of fuels, which may lower the EBITDA margins, and lower Phinia stock valuation. Besides, changes in labor conditions or changes in the environmental laws could lower both the FCF margins and the demand for the stock.

My Conclusion

Even taking into account recent lower than expected EPS GAAP, Phinia Inc. may offer significant upside potential to shareholders. Significant geographic diversification, which may bring lower net sales revenue volatility, improvement of the commercial vehicle market, and adoption of hydrogen solutions may also bring further net sales growth.

In sum, if the recent restructuring efforts and lower headcount growth do not ruin future FCF growth, I believe that Phinia Inc. is a must-follow stock. There are obvious risks arising from its relationships with BorgWarner, and changes in the environmental regulation could affect the stock. However, Phinia Inc. stock is currently very undervalued.

")

")

")

")

")

")

: A Robust Business Facing A Secular Threat")

")

")