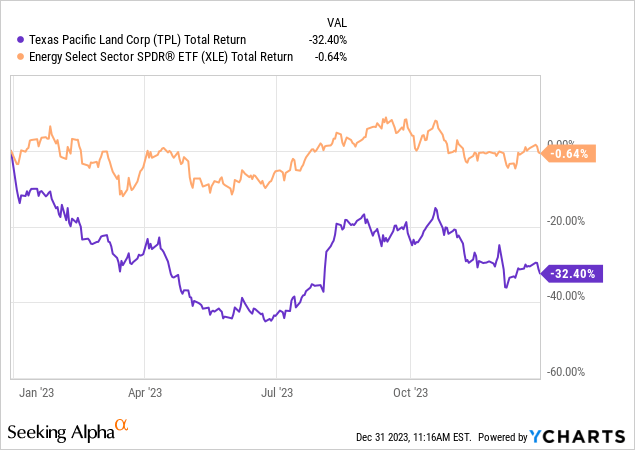

Texas Pacific Land Trust’s (TPL) investors had a very tough 2023. It was rough to see the broader markets power higher driven by tech. However, a land investor playing on the oil and gas theme can look past that. One did expect TPL to suddenly announce that they had found an AI themed play on their exploration lands. What was really painful, was to see TPL underperform Energy Select Sector SPDR (XLE) by a whopping 32%.

Data by YCharts

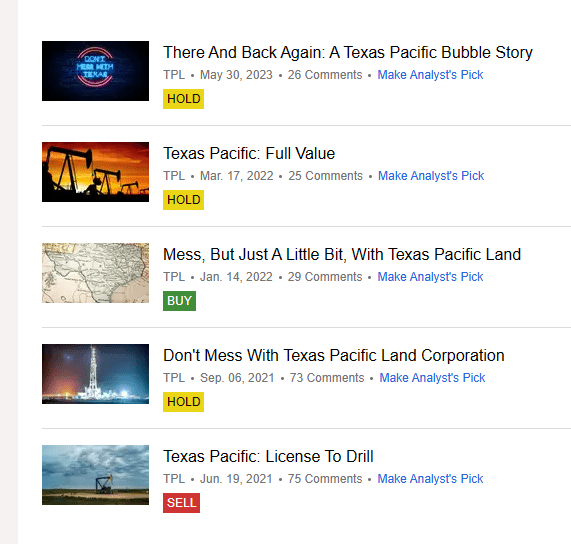

Our own coverage of TPL has been pretty straightforward. It started with a Sell/Short Sell rating at $1,550 in June 2021. We then suggested investors go neutral at $1,250 and we even had the temerity to suggest a buy at $1,050 in January 2022.

Seeking ALpha

In general, over these timeframes, these trades have worked far better than buying and holding as the stock is flat over the last 30 months. We examine the valuation today and tell you why we think TPL will have it rough in 2024, at least relative to the other opportunities that present themselves.

What Is TPL Worth Today

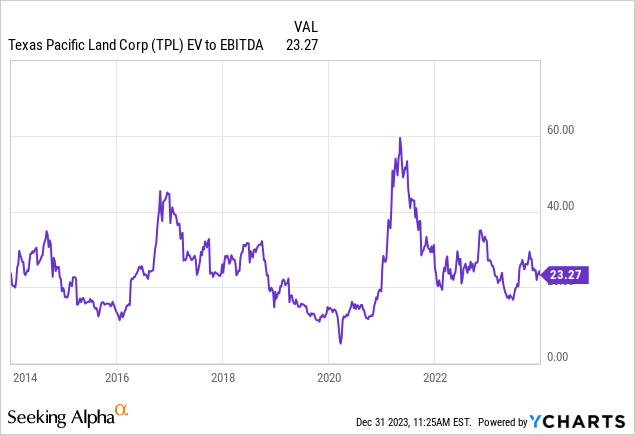

The crowd is probably looking at this from the perspective of the EV to EBITDA and based on the last decade, TPL does not look expensive.

Data by YCharts

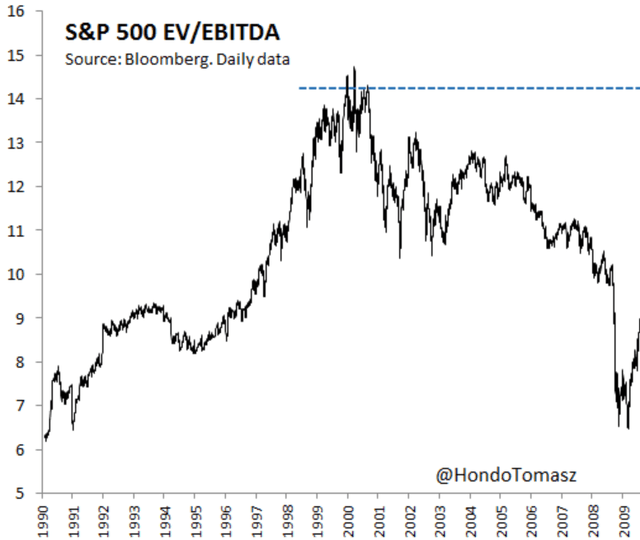

There are a few nuances lost when we just pull up the chart of TPL relative to where it has been. The first being that the bulk of that history was during ZIRP (Zero Interest Rate Policy). Even there, the stock did trade far lower on EV to EBITDA basis in 2016. Let’s not forget that 2016 marked a low for Crude oil and TPL’s EBITDA was quite depressed. Even off those low numbers, the market priced it pretty cheaply relative to where we are. So the potential exists for this to trade at 16X EV to EBITDA today, and that will be a painful journey. Even that 16X will be a premium to the S&P trading at 14X EV to EBITDA. Let us add on here that the S&P 500 itself peaked at 14X EV to EBITDA in 2000 and did not surpass those index levels till more than 15 years later.

Hondo Tomasz

So TPL still rings in expensive by any conventional measure.

But the real reason TPL is so expensive today is that the growth story is more or less over. You could justify paying 25X EV to EBITDA during ZIRP when TPL was a tiny company and its lands were still being explored. There was growth to be had. That growth is now coming to a standstill. The latest quarter showed that all three categories of energy products declined year over year.

TPL 10-Q

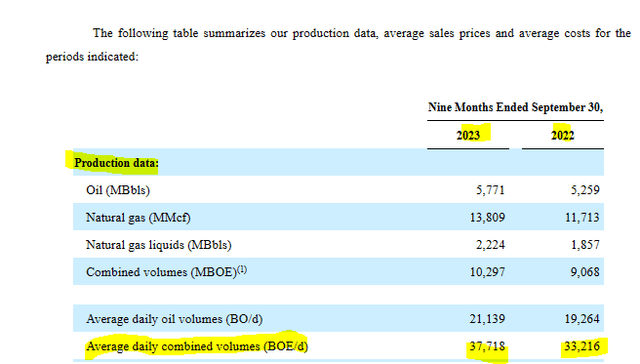

Yeah, you can run with “buy land, they are not building any more” mantra, but this is not as straightforward as that. While Permian production for Oil, Natural Gas and Natural Gas Liquids, hit new high highs in 2023, TPL’s base showed a 7% decline.

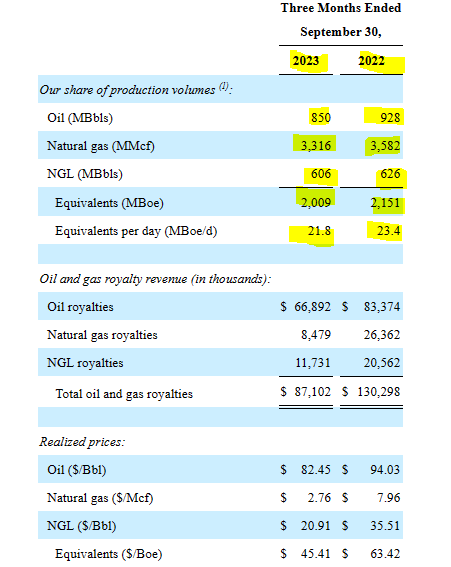

Here is quick look at Freehold Royalties’ (FRU:CA) production data for the same quarter. A small 3% increase. Nothing groundbreaking, but solid nonetheless.

FRU Q3-2023

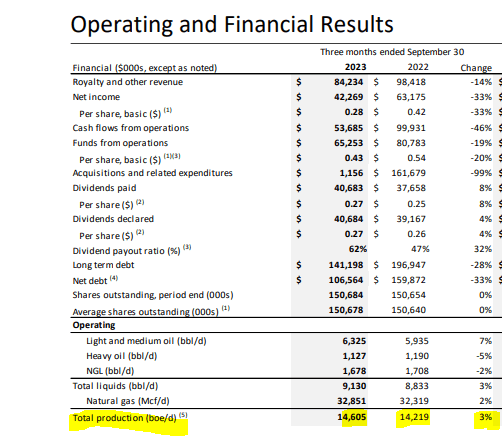

What about Viper Energy, Inc. (VNOM)? They did better so far in 2023 and production has been growing nicely.

VNOM Q3-2023

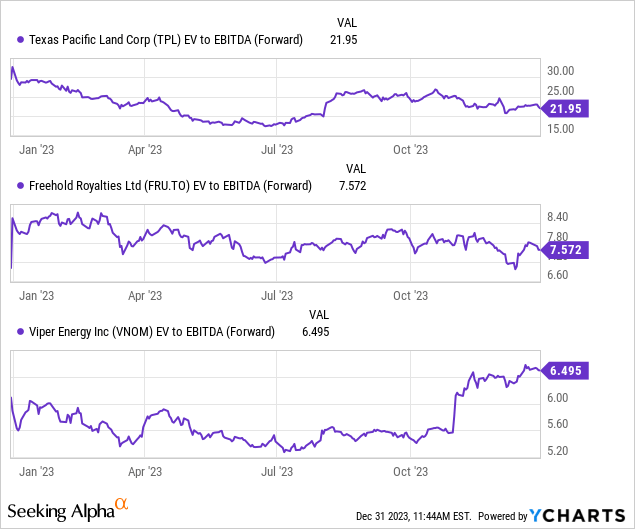

We see things from a big picture perspective. We are not going to quibble over whether TPL will generate a 7% decline or a 2% decline. We won’t bother forecasting whether VNOM’s acquisitions will be accretive or not. But we just want to draw your attention to this. What rational reason is there to pay 3X the EV to EBITDA multiples for a declining royalty production compared to one that is growing?

Data by YCharts

Humor us please.

Verdict

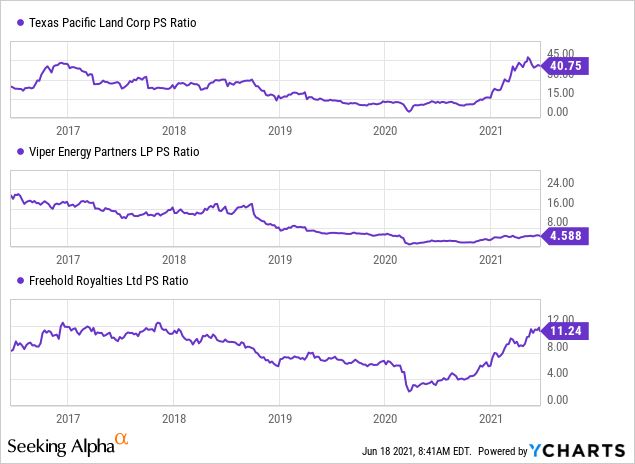

If these arguments sound exactly the ones we made when we first wrote why you should not buy TPL, back in 2021, consider us guilty as charged. There were 75 comments on that one and most were not comprehending the giant hurdle of relative valuation. In fact, here is a snippet of what we wrote back then as we stared in disbelief at TPL’s relative valuation. Note the two companies we identified back then as well.

The absurdity of the multiple can also be seen against some similar royalty interest companies.

Y-Charts from 2021 Article

Do keep in mind that TPL itself identifies 21 years of drilling inventories. Paying 41X sales for a company with 21 years of drilling inventories is definitely high up on the list of absurdities we have seen in this market.

Source: License To Drill

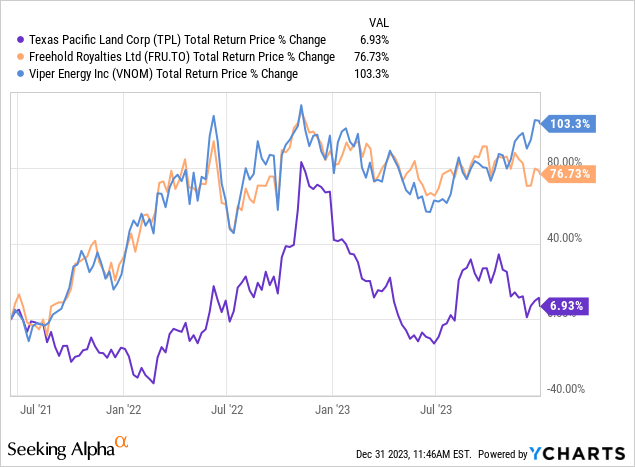

30 months later investors have got proof that valuation does matter and the past is not always the future. TPL has been taken to the cleaners by the other two royalty plays.

Data by YCharts

So this brings us to recent drama regarding TPL where the company had a standoff with its largest shareholder, Horizon Kinetics. That lawsuit was about whether or not TPL could find a way around issuing new shares. TPL won that.

Texas Pacific Land Corporation announced today that the Delaware Court of Chancery (the “Court”) has ruled in favor of TPL in the litigation between the Company and Horizon Kinetics LLC, Horizon Kinetics Asset Management LLC, SoftVest Advisors, LLC and SoftVest, L.P. (collectively, the “Investor Group”), in Texas Pacific Land Corp. v. Horizon Kinetics LLC, (C.A. No. 2022-1066-JTL) (Del. Ch.). On December 1, 2023, the Court ruled that the Investor Group should have voted with the Board’s recommendation on Proposal 4, the Company’s proposal to increase the number of authorized shares of common stock (the “Share Authorization Proposal”) at the 2022 Annual Meeting, under the terms of the June 2020 Stockholders’ Agreement with the Company (the “Stockholders’ Agreement”). The Court has deemed the Investor Group’s shares to have been voted in favor of the Share Authorization Proposal, which has been deemed approved by stockholders.

As previously disclosed, once a final order is entered and an amended charter is filed, the Company intends to use a portion of the newly authorized shares to affect a stock split of the Company’s common stock in the form of a stock dividend, and the Court has conditioned the Share Authorization Proposal on such a stock split. In addition, the Share Authorization Proposal increases the number of authorized, unissued shares of common stock.

Source: TPL

Now, we have seen many investors gripe and moan about this and this is a tad confusing. From our perspective, TPL is ridiculously overvalued relative to the alternatives. Similar royalty plays trade at a third of its valuation. Proper E&P companies trade at a fifth of its valuation. So TPL should be issuing stock to possibly buy other assets or companies. If we were in charge of TPL, we would be issuing stock every day. We might even hire someone to do it in case we missed an opportunity while taking a siesta. In fact, this might be the prototypical case of “you snooze, you lose”. At 22X EV to BITDA, there are zero reasons to not issue stock. Management knows it and investors who favor math over storytelling, will favor it as well. We rate the stock a “hold” solely as we are believers in a much higher oil and gas price environment in the coming years. On a relative basis, the last 30 months were just a warm up of what returns you will get compared to anything in the royalty or E&P space.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")

")

")

")

")

: A Robust Business Facing A Secular Threat")

")

")