")

")

- Las Vegas could see a record 400,000 arrivals over the Super Bowl game weekend.

- Macau could likewise see 200,000 coming for Chinese New Year.

- MGM’s footprint in both markets plus BetMGM triggers the possibility of a big earnings beat in 1Q24.

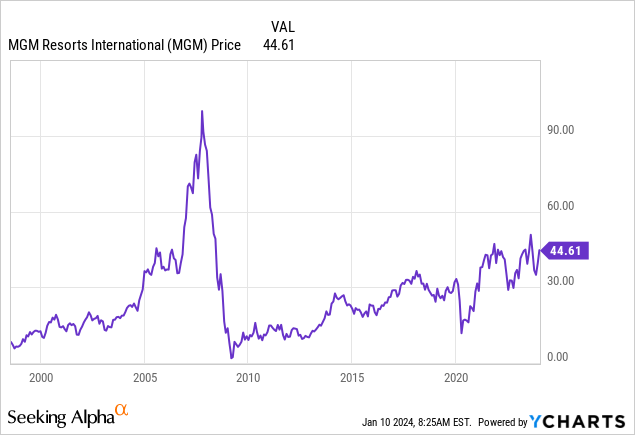

On Dec. 7 we put a price target of $47.85 on MGM Resorts International (NYSE:MGM) when it was trading at ~$40. At writing the stock is $45. Analysts are looking for $0.64 in earnings for 1Q24. While I don’t think it’s wildly conservative, I do believe it does not adequately bake in what I see as a blowout quarter formation.

For that reason among others, I’m raising guidance on MGM to $64 by the end of 1Q24 in the belief that the incredibly serendipitous gaming calendar ahead holds potentially explosive potential for MGM, among some others, among many verticals.

MGM at its current price is significantly undervalued.

Super Bowl in Las Vegas Feb. 11.

Above: Handle will break all records but revenue windfall will come from a town booked as near 100% as possible. MGM will disproportionately benefit.

MGM’s eight strip hotels with an excess of 6,000 rooms will be at near 100% occupancy with average rates that could be in the $500 to $700 per night for regular rooms — let alone suites. Add dining, nightclubs, and shopping, of course. Note that our sources on the ground plus our archived data from our own files saved from during our career we believe the 450,000 estimated arrivals will have at least a 23% higher gaming profile than tourists or conventioneers

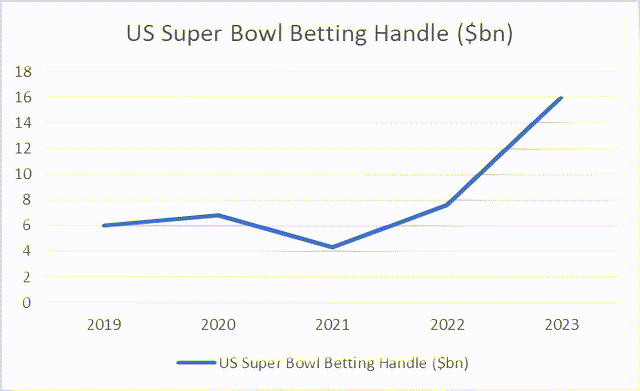

Super Bowls of the past remain one of the top calendar events for Las Vegas along with New Year’s Eve – when the game was played elsewhere. It generally drew 300,000 visitors. Sports betting was a rationale for bettors before the 2018 legalization surge all over the country.

But in total sports bets never amounted to anything like the money generated by visitation itself. Last year, the sports books handled ~$150m in wagers — chump change by what we can expect the top five legal platforms to handle nationally this year. This first time ever for the game to be played in Las Vegas brings a collision of the worlds of gambling, entertainment, and big-time sports far greater than the next biggest Vegas sports event draw: The Final Four. We believe the game will blow that event out of the water. There has never been a sports event that has brought those three worlds together in a single weekend.

Yes, we can expect some variants depending on the heft of the two teams and the home market. For example, if the Dallas Cowboys emerge from the NFC, put that down a big time plus. If two teams from smaller markets make it to the big game it could have a dilutive impact — except if the AFC team is the Kansas City Chiefs which could well include the presence of Taylor Swift in Vegas that would skyrocket the event beyond any forecast.

Above: As an example of the strong recovery cycle of Vegas gaming, we note above last November’s upside which has continued since breaking all records for both gaming and non-gaming revenue.

Allegiant Stadium will clearly be sold out to the rafters with tickets running into high three or even four figures. But that’s 65,000 people. But as we know, the casino business is marketed by segmentation. So while the top casino players will likely be at the game, the modest-budget players won’t be forgotten. MGM for example has its 17,000 capacity Garden Arena to show the game on a giant screen with attendees being more than adequately served with food, drink, and live entertainment. Add the sports book crowds and you have a recipe for a historic weekend ahead.

Chinese New Year Feb. 10

Just 24 hours before the big game an estimated official Macau government database predicts between 175,000 and 200,000 visitors, a population with the highest average gaming proclivity on the globe. MGM’s two properties in that market are ranging ~a 9% to 11% share of market. All first-class hotels in the market are likewise expected to hit occupancy in the mid to high 90%. Both properties have a combined total of 2,000 rooms. Average budgets according to our sources there estimate, the $600 per person in gaming speed pre-covid will be surpassed. But the player mix will be different.

Largely shrunk to low single percentages will be the VIP/junket segment. But the powerful surge in mass and premium mass revenue growth will more than compensate for much of the loss in VIP. We don’t totally rule out VIP as a factor since Chinese New Year does have the compelling allure for that segment of play as well as due to big time A list entertainment.

The two events exploding within days of each other will set the stage we believe for a powerful earnings performance in 1Q24 for MGM in particular. Remember, MGM is a major presence in Las Vegas, owns two top properties in Macau and thirdly sits right behind the two leadership sports betting sites, DraftKings (DKNG) and FanDuel (FLUT) – debuting on the NYSE late this month. We expect a big time earnings beat for 1Q24 based on two elements. One, the performance achieved by the double dynamite of two major gaming events for February. And two, the momentum for MGM is moving beyond several factors that bruised their earnings late last year.

MGM’s 3Q23 results generated $2.1B in revenue for the Las Vegas segment down 10% largely due to the disposition of the Mirage and Gold Strike properties as well as the black swan cyberattack in September which also contributed to a 10% decline in EBITDAR for the quarter.

The company also reported it expected to continue its stock repurchase program into 2024 with another $1b authorized.

At the same time, its 50% owned sports betting site BetMGM had reached guidance revenue of $1.80b to $2b with the expectation that the business had turned profitable by the second half of the year. Add that to the strong post-COVID performance of MGM China and you have a picture going into 2024 of a company with many catalysts ahead and no known tailwinds in any of its segments.

Another pending catalyst

The New York State legislature has authorized the issuance of three full-service casino resorts to be developed in the downstate metro area. The New York market is the largest in the US with near 20m in population. MGM currently operates the Empire City Casino in the city of Yonkers just over the NYC border. There are perhaps five at best credible bidders for one of the three licenses to be issued. They include Las Vegas Sands (LVS) Caesars (CZR) and the operators of the other lottery terminal property in metro NY, Genting.

None of our sources believe there are can’t-miss bidders in the loop here, but all do agree that MGM has to be considered among those with the best odds to prevail. The reasoning is simple: MGM is one of two existing operators in the area already with deep networks in the city. As do all bidders it already has developed a plan for a massive expansion and overhaul of its Empire City property should they win a license. The plan includes an expansion of the 160,000 square foot casino and the development of a 5,000-seat arena for major entertainment events.

(Note: Post COVID and related to a sharp decline in attendance to Broadway shows among suburbanites due to fears about crime, venues close to the city with the financial heft to stage Broadway quality shows and events will thrive going forward).

Geographically the Yonkers site is very close to the core population concentrations of downstate New York, Northern New Jersey and Southern Connecticut.

MGM expects a decision to come down sometime before spring. If it includes MGM, we see it as a significant catalyst for forward revenue and earnings. The rationale here is this: Right now Empire City is as noted a lottery terminal casino. Under the new license, MGM would not have to wait until its construction and expansion plans are completed downstream. It can immediately exchange its lottery slot terminals for standard slot machines and add live table games aimed at generating immediate gains in revenues.

Conclusion

We have long posted our strong bullish sentiment on the shares of MGM believing that its global reach in Asia, its fortress footprint on the Las Vegas strip, its key regional properties, and its occupation of third best market share in US sports betting makes it undervalued.

Looking at the last several earnings reports we have seen one-time events damaging a forward thrust of earnings beats and subsequent movement of the shares to what we believe is a much higher valuation.

As a general guide we looked at alpha spreads DCF valuation of MGM to give some context to our upgraded PT.

They put base case value at $41.92, very close to its price at this writing.

They put best case value at $114.34 which of course assumes surging FCF projected to a terminal date at least five years ahead. Having been in the business for so long and watched the play of forecasts often running to wild extremes by the analyst community at times, we are loathe to join the ranks of fearless forecasters yet. However, we clearly see MGM moving forward now with powerful momentum generating from the gifts of the early February gaming calendar.

We don’t think this is as yet widely understood as being the possible catalyst that could be putting a higher floor on the base case noted above. And for that reason, we’re raising guidance on MGM as noted.

Read the full article here

")

")

")

")

: A Robust Business Facing A Secular Threat")

")

")