")

Investment Thesis

Confluent (NASDAQ:CFLT) is making all the right moves. More specifically, Confluent is on a straight path to improving its bottom-line profitability.

However, to improve its profitability, Confluent is having to sacrifice its growth rates.

Consequently, I estimate that confluent isn’t particularly cheap, at 160x forward non-GAAP operating profits.

Altogether, Confluent is emblematic of the premium investors are having to pay to participate in this space. What’s more, as I discuss in the analysis, Confluent’s 2025 will be its first year as a self-sufficient business. This means that beyond 2025, we should expect its profits to rapidly increase.

Rapid Recap

In my previous analysis, I turned bullish on CFLT for the first time. I said,

Confluent is a contentious stock. The business’s growth rates are moderating. More specifically, despite management declaring that this business can grow at 30% CAGR, including the presumption of revenue beats each quarter of 2024, its growth rates will still be sub 30%.

However, Confluent’s underlying profitability is expected to ramp up significantly in 2024, so that investors can see a path for Confluent to exit 2024 with 4% non-GAAP operating profits and climbing higher into 2025.

Author’s work on CFLT

The premise then, and now, is for the most part unchanged. But I was caught slightly off guard by the pace that this business is decelerating its growth rates. Nevertheless, I maintain that investors are throwing the baby out with the bath water.

Confluent’s Near-Term Prospects

Confluent provides tools for businesses to manage and analyze large amounts of data in real time. Using open-source Kafka technology and their Confluent Cloud service, they help companies process data continuously, allowing for quick decision-making. Confluent competes with Amazon’s (AMZN) AWS Kinesis and Microsoft’s (MSFT) Azure Stream Analytics, among others.

Confluent’s near-term prospects are fair, with Confluent reporting a 25% y/y increase in total revenue. This reflects the company’s effective execution in a stabilizing macro environment. The company has also focused on transforming its sales compensation to emphasize incremental consumption and new customer acquisition, resulting in the addition of 160 customers, the highest sequential growth since Q1 2023.

Confluent’s product innovation is robust, with significant features such as Tableflow and Flink, which enhance data integration and real-time processing capabilities.

On the other hand, Confluent faces challenges related to its slowing growth rates and the broader economic environment. For example, the pace of new software development initiatives has only slightly picked up from last year, which had a heavy focus on cost optimization. This cautious approach from customers could limit the speed at which Confluent can expand its market share.

Plus, I’ve often found that companies make the transition to consumption-based as a last-ditched attempt at leaving their customers with a large bill, while delivering investors solid revenue growth rates. But in my experience, this is a ticking time bomb. An example to support my argument include Snowflake (SNOW) and MongoDB (MDB), where customers are less than pleased with a rapidly growing bill for using these platforms, and customers are busy looking towards alternative offerings.

Given this balanced context, let’s now analyze its fundamentals.

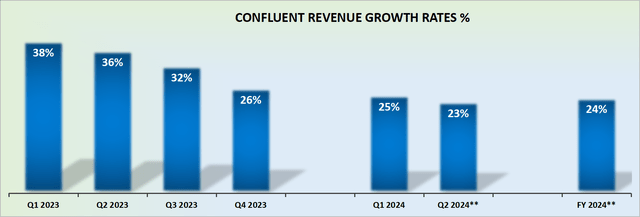

Revenue Growth Rates Moderate to Approximately 25% CAGR

CFLT revenue growth rates

Previously, on the back of its Q4 2023 results, I said,

Confluent has provided guidance indicating a CAGR of approximately 25% for the upcoming year. However, considering that 2023 presents a somewhat less challenging hurdle for Confluent to surpass, coupled with the historical trend of Confluent’s management exceeding revenue consensus by approximately 2% to 3% (see below), this strengthens my belief that there is a very high probability that Confluent will meet or slightly exceed its present guidance. Consequently, this could lead to achieving a 27% CAGR in 2024.

However, now that management has updated its guidance, and yet, the growth rates are still approximately 23% to 24% CAGR, I suspect that Confluent is going to struggle to reach 27% y/y revenue growth rates this year.

And that’s a problem. After all, investors were willing to buy into management’s narrative, provided that they could deliver very strong growth rates.

Because if they haven’t got the growth to support their narrative, then, investors will start to question whether it makes sense to pay a premium for this stock. And given this segue, let’s now discuss its valuation.

CFLT Stock Valuation — 160x Forward Non-GAAP Operating Margins

Confluent’s Q2 2024 guidance points to approximately a negative 1% non-GAAP operating margin. This is a slightly more than 800 basis points improvement in profitability relative to the same period a year ago.

Similarly, 2023 finished with non-GAAP operating margins of negative 7.4%, while this year’s non-GAAP operating margins point to approximately 0%, meaning there’s approximately 750 basis point improvement in profitability in 2024 relative to 2023.

Consequently, given that Confluent’s non-GAAP operating margins are evidently improving at around 700 to 800 basis points relative to last year, I estimate that there’s enough potential for Confluent’s non-GAAP operating margins to improve next year by approximately 300 to 400 basis points.

In practice, this means that assuming that next year’s topline grows by around 23% y/y, this would see Confluent’s non-GAAP operating profits reaching around $50 million. Altogether, this means that Confluent is priced at 160x forward non-GAAP operating profits.

Clearly, this is far from cheaply valued. But there again, we have to keep in mind that this will be only the first year of profitability for Confluent. The business at that juncture will be self-sufficient and generating some free cash flow. After all, these SaaS businesses are rarely cheaply valued, since investors crave the predictability of their growing revenues. In short, that’s just the going price.

The Bottom Line

In conclusion, while Confluent demonstrates a clear path to improving its bottom-line profitability, this comes at the expense of its growth rates, resulting in a valuation of 160x forward non-GAAP operating profits.

Despite the company’s robust product innovation and effective execution leading to a 25% y/y revenue increase, its moderating growth rates present a challenge.

However, with 2025 expected to be its first year as a self-sufficient business, Confluent’s profitability should rapidly increase beyond 2025.

Although the current valuation is steep, reflecting the premium for participating in this sector, the potential for sustained revenue growth and profitability makes Confluent a reasonable investment. Not the most compelling investment given its valuation, but satisfactory.

Read the full article here

")

")

")

: A Robust Business Facing A Secular Threat")

")

")

")