")

Nothing has caused more issues than the progress or lack thereof of both EBITDA (since the acquisition) and its place in the coming growth for Warner Bros Discovery (NASDAQ:WBD) since the last article. Management has since done a bunch of presentations to try and smooth out the process of going from “cutting like mad” because the acquisition literally had no cash flow (or definitely nothing close to enough) to growing the business. Mr. Market is upset that growth has not occurred from the start while fretting about that lack of growth on the effect of EBITDA and cash flow. Put Mr. Market down as less than pleased with the whole situation. But also realize that if management follows through with the plan, and more goes right than wrong, Mr. Market may well become a fan.

Stock Price History

All of this confusion has, of course affected the stock price.

Warner Bros Discovery Common Stock Price History And Key Valuation Measures (Seeking Alpha Website June 10, 2024) Warner Bros Discovery Common Stock Price History And Key Valuation Measures (Seeking Alpha Website May 31, 2024)

Never mind that board member John Malone gave an interview stating that this would take a while to work out because things were worse than management expected. He also noted that he sold puts to support management.

Mr. Market has clearly been disappointed from the start (as shown above). Sometimes, a large acquisition is more like building a house except for the fact that you receive a value report from the market every day. That value report can lead you astray as to the progress management is making. This has led management to the latest “road show”.

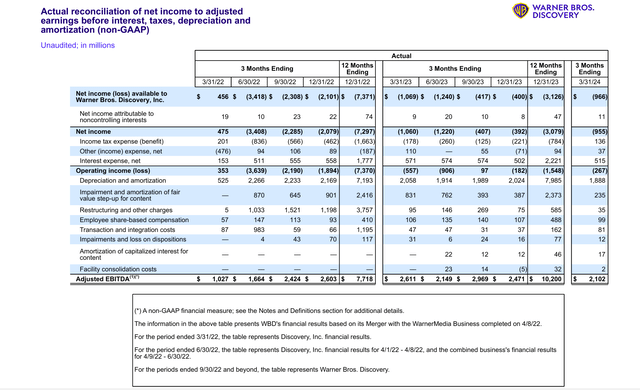

EBITDA Progress And Free Cash Flow

The last article mentioned management’s frustration over the market impatience with reconstructing the corporation in a way that improves profitability and leads to growth.

The market responded by shifting the conversation to revenue growth and EBITDA.

Warner Bros Discovery Adjusted EBITDA Progress (Warner Bros Discovery First Quarter 2024, Earnings Supplemental Calculations)

Note that EBITDA definitely grew year over year. But there was some concern that the quarterly comparison turned negative beginning with the fourth quarter.

This is a company where earnings will be heavily influenced by movie (or games for example) hits. Last year there was a very successful game that was not replicated for the fiscal first quarter. Before that there was the double strike (among other issues). Therefore, quarterly comparisons can definitely swing wildly, and it really will not mean much.

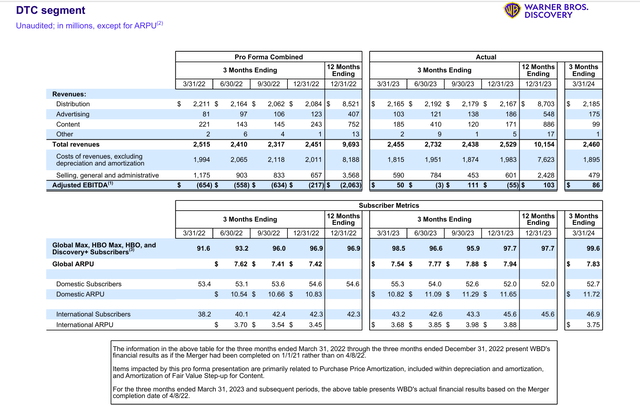

One of the things that impacted EBITDA in the previous fiscal year was that DTC moved from losing billions to nearly breakeven (as covered throughout the year in previous articles.

Warner Bros Discovery DTC Trend Results (Warner Bros Discovery First Quarter 2024, Earnings Supplemental Calculations)

One of the things to remember about this is that the improvement in DTC that is shown above came a year ahead of schedule. The comparisons could well be flat or vary slightly either way because the growth plan is on schedule. But it is just now being presented in the latest conference presentation.

Now the market pretends to be tired of hearing “the same old thing” when the real reason is there is no dramatic improvement to match the previous fiscal year. Yet the absence of those big losses was a factor in the debt repayment being far ahead of the original schedule.

Management likely raised some goals where it could when something like this happens. But to expect the “full next step” which is likely a growth strategy a year early because the financial improvement occurred ahead of time is likely not reasonable. Instead, it is reasonable to expect some flat results until the next step gets underway as planned.

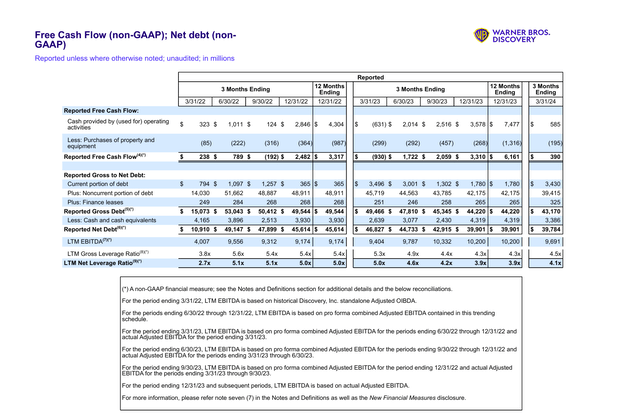

Free Cash Flow

Also, it is important to note that “you cannot spend EBITDA”. Therefore, EBITDA progress has to be compared with cash flow and free cash flow progress. Therefore, you, the investor need decide if you agree how the GAAP number was spent and if you agree with the non-GAAP free cash flow calculation as a spendable number.

Warner Bros Discovery Free Cash Flow And Related Trends (Warner Bros Discovery First Quarter 2024, Earnings Supplemental Calculations)

Ever since the first quarter of fiscal year 2023, the free cash flow comparison with the previous quarter has been improving. For an acquisition the size of the one made here, that is a tremendous improvement in a time period that few managements can match. This has funded an unexpected robust debt reduction plan that has given the company considerable financial flexibility earlier than some of us expected.

Note especially that the first quarter showed a more than $1 billion cash flow improvement over the previous fiscal year. Many were focused on EBITDA. But the cash flow improvement shown above is spendable while EBITDA is not.

Also note that the company has paid down roughly $10 billion of long-term debt since the acquisition in 2022. Since the close of the quarter, management has called still more debt. This led to a comment in the latest conference call about repaying roughly $13 billion in debt since the acquisition.

Deleveraging Strategy

Probably the single most important objective has to be to generate cash to deleverage. Management has mentioned in several conference calls and presentations that cash was not important before the acquisition. As a result, they discovered items that needed to be billed combined with other items that needed to be collected. This has likewise helped the deleveraging process.

Mr. Market may not care about this as it is a “one-time” or “not repeating” item. However, the repayment of debt gives management a lot of flexibility. It was mentioned in the latest presentation that management will look at acquisitions. The leverage ratio below 4 likely gives management the option to do just that. Management will likely have the debt ratio below four with the next quarterly report.

Once that happens then other business strategies will rise in importance.

Business Strategy

The latest conference centered upon the idea that management will now grow the business. That has been talked about ever since the acquisition was made.

Clouding the issue was a lack of cash flow of the acquired assets. That had to be fixed first. Management therefore redirected efforts towards profitability with cost controls and proper accounting. Clearly systems had to first be constructed for that. This has led to management frustration with the market more than once.

But what is emerging now is a market attitude that the company did not grow, therefore, it cannot grow. Yet it is very necessary to have the proper strategies with support systems in place before profitable growth can occur.

To this end there was a conference discussion about bundling as this company has long been in the forefront of discussing that concept. It also took some time to come up with a rational growth strategy after the support systems came into existence. With a big company this takes more time than the market had patience for.

Now management laid out those growth plans during the conference presentation. To a certain degree, these plans have also been discussed in conference calls and other presentations. What is different is that after two long years of waiting, some of those plans are launching.

Mr. Market was yawning like this was too late. But entertainment is a very fractured market with no one really controlling a significant part of the market. Therefore, good product is needed, or the growth would fail. It also means that there may not be consolidation due to the fractured nature of the market. This could change as the streaming market ages. Basically, anyone with a competitive product can “jump-in” at any time right now. Barriers to entry are low to non-existent in some cases. The consumer has a lot of choices as a result.

Despite the market reaction, there is every chance that the company now has the financial flexibility to adjust its strategy once that strategy is launched. Money can do wonders. The fact that the debt has been paid far ahead of time now gives management flexibility to execute the coming growth strategies that leveraged purchases often do not have.

As far as when these strategies will take-over to lead the company to more profitability as the effects of the initial deleveraging effort (and building support structures) fades, that can vary. Most likely it will catch the market by surprise.

The market has been bored to death so far with the initial steps. But if those steps are done correctly, the market will likely adore what comes next.

Sports

The market has been concerned with the NBA contract negotiations for some time. But management has brought up that their sports coverage (or delivery) has been a worldwide organization for some time. Therefore, the loss of any one perceived major item, like the NBA contract, is unlikely to prove to be a long-term issue.

A contract for the French Open Tennis tournament was just announced. This is precisely the kind of announcement that would lead to a necessary rebuild (or replacement of the loss) of the sports coverage should the NBA contract be lost. It would of course take several of these as the NBA contract is far more significant. But as a worldwide business, there are many things that can eventually offset the loss of the NBA contract.

Of course, that loss has not occurred despite market worries. But the existence of a worldwide organization is yet another benefit that may help during the negotiations. There could well be economies of scale that competitors do not have and other benefits as well.

Summary

The initial steps of the acquisition have been a painful process with a lot of negative results catching the attention of Mr. Market. This even has Mr. Market fretting about the free cash flow progress because he thinks the business will not grow (mostly because it has not).

But it’s hard to measure the growth of the remaining businesses because a lot of unnecessary “tasks” were cut. This led to a shrinkage by eliminating nonessential and unprofitable parts of the corporation while improving the core operations that are the future of the company. This kind of progress the market does not see currently and certainly cannot measure whereas the losses and mistakes appeared to be very real.

This is a strong buy based upon the idea that management has done what it had to, and it was accomplished to correctly support the coming growth that the market will very much like. Lost in all of the worry is the very improved debt ratio at a rate that was completely unexpected.

While the market clearly doubts a lot of the latest management conference presentation, the market will remember what was said should management perform according to the guidance set. That could lead to a considerably higher stock price later.

Risks

The latest strategies, like launching “MAX” and bundling could fail or run into unexpected problems. They likewise could fail to meet management expectations. As the CEO and others noted, they intend to keep working with the new ideas until satisfactory returns are obtained. That may likewise take longer than the market has patience for. It is possible, but unlikely that it never happens, and the stock price never recovers or exceeds the price before the acquisition.

The potential lack of success in renewing the business relationship with the NBA is also weighing on the future of the stock price. There can be no assurance that a loss of the contract can be offset by enough business elsewhere.

The movies are currently running ahead of expectations. There is absolutely no assurance that will lead to a good year or a good next year((s)). Similarly, there is a risk that games will never have another “hit” game.

Management claims to have found the material “skeletons in the closet” that needed some major actions. There is no assurance that there will not be yet another material discovery in the future.

The loss of key personnel could set back company plans materially.

Read the full article here

")

")

")

: A Robust Business Facing A Secular Threat")

")

")

")